Blog | Paper Assets

The Great Deceleration

August 01, 2013

The cover of The Economist magazine this week shows sprinters representing Brazil, Russia, India and China (the BRICs) stuck in the mud. The cover’s caption reads: “The Great Deceleration”. The lead story points out that, relative to 2007, the rate of economic growth has decelerated from 14.2% to 7.5% in China, from 10.1% to 5% in India, from 8.5% to 2.5% in Russia and from 6.1% to 2.5% in Brazil. The article concludes that this emerging market slowdown is a turning point for the world economy, but not the beginning of a bust.

I was aware of the sharp slowdown in these economies. You may recall I wrote two blogs about the end of the great China boom after a trip there with Robert and Kim last summer. What I did find surprising about this story is that The Economist failed to even mention the real (and obvious) reason these economies have slowed.

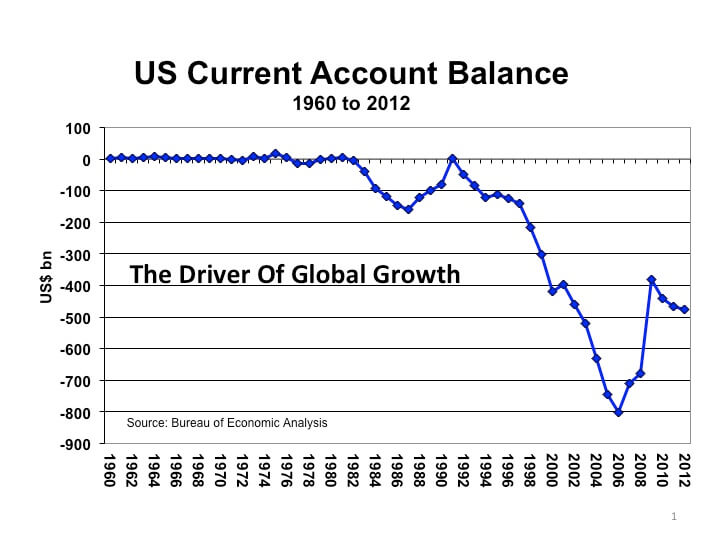

The “great deceleration” has been the direct result of the sharp correction in the US Current Account deficits – just as the great acceleration that preceded it was brought about in the first place by the extraordinary and unprecedented blowout in that deficit between 1991 and 2006.

The US Current Account deficit reflects the extent to which the United States buys more from the rest of the world than the rest of the world buys from the United States. Between 1991 and 2006, the deficit increased from zero to $800 billion. That US buying binge created the greatest global economic boom in history – and the BRICs were the major beneficiaries of that boom. It should come as no surprise then that those economies have slowed so significantly now that the US Current Account deficit has contracted by 40% from its peak.

The Economist should have explained that in its first paragraph and then gone on to consider, first, whether the US Current Account deficit will begin to widen again and, second, what the consequences for the global economy will be if it doesn’t.

Allow me to fill in the gaps. The US Current Account deficit is not likely to grow significantly enough in the foreseeable future to rescue the BRICs. US economic growth is just too weak. The economy is weak because credit growth is weak. Neither is likely to revive in the short run.

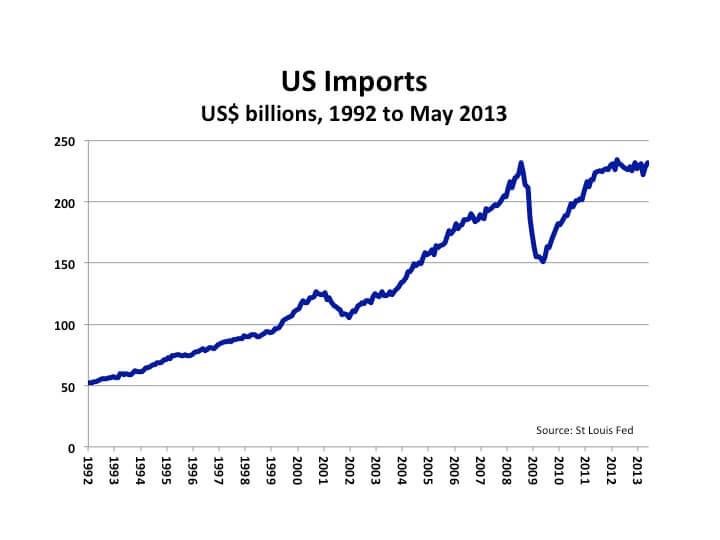

Since World War II, credit growth has driven economic growth in the US. Between 1952 and 2008, every time credit growth (adjusted for inflation) grew by less than 2% the US fell into recession. Credit growth is below that 2% threshold now. Quantitative Easing has kept the country out of recession, but just barely. During the first half of 2013, the economy grew at an annualized rate of only 1.4%. Over the next 12 months, credit growth is unlikely to pick up because the government is in the process of sharply reducing its budget deficit. That means it will borrow less during the quarters ahead. Consequently, the US economy is likely to remain weak. US imports, which used to drive global economic growth, have been flat for the past 14 months. And a near term turnaround in US demand for foreign goods does not appear likely. Therefore, the US Current Account deficit should remain roughly unchanged.

The Economist’s optimism that this is “not the beginning of a bust” is also surprising. Looking back across economic history, it’s hard to find a boom that didn’t bust; and, generally, the bigger the boom has been, the bigger the bust that followed it. The BRICs Boom has been one of the biggest ever recorded. The odds are they will experience something considerably worse than economic deceleration before this super-cycle has fully played itself out.

Original publish date:

August 01, 2013