Blog | Personal Finance

The World’s Not Large Enough For China

June 15, 2016

China’s economy is in trouble. That’s bad news for everyone, not just the Chinese. Worst still, China’s troubles are only just beginning. Its economic slump is likely to be deep and protracted. This blog will discuss the causes behind China’s Hard Landing.

China’s economy is freakishly unbalanced. Investment (technically, Gross Fixed Capital Formation) makes up 44% of China’s GDP, whereas Household Consumption makes up only 38% of GDP. For the world as a whole, Investment makes up just 24% of global GDP, while Household Consumption makes up 57%.

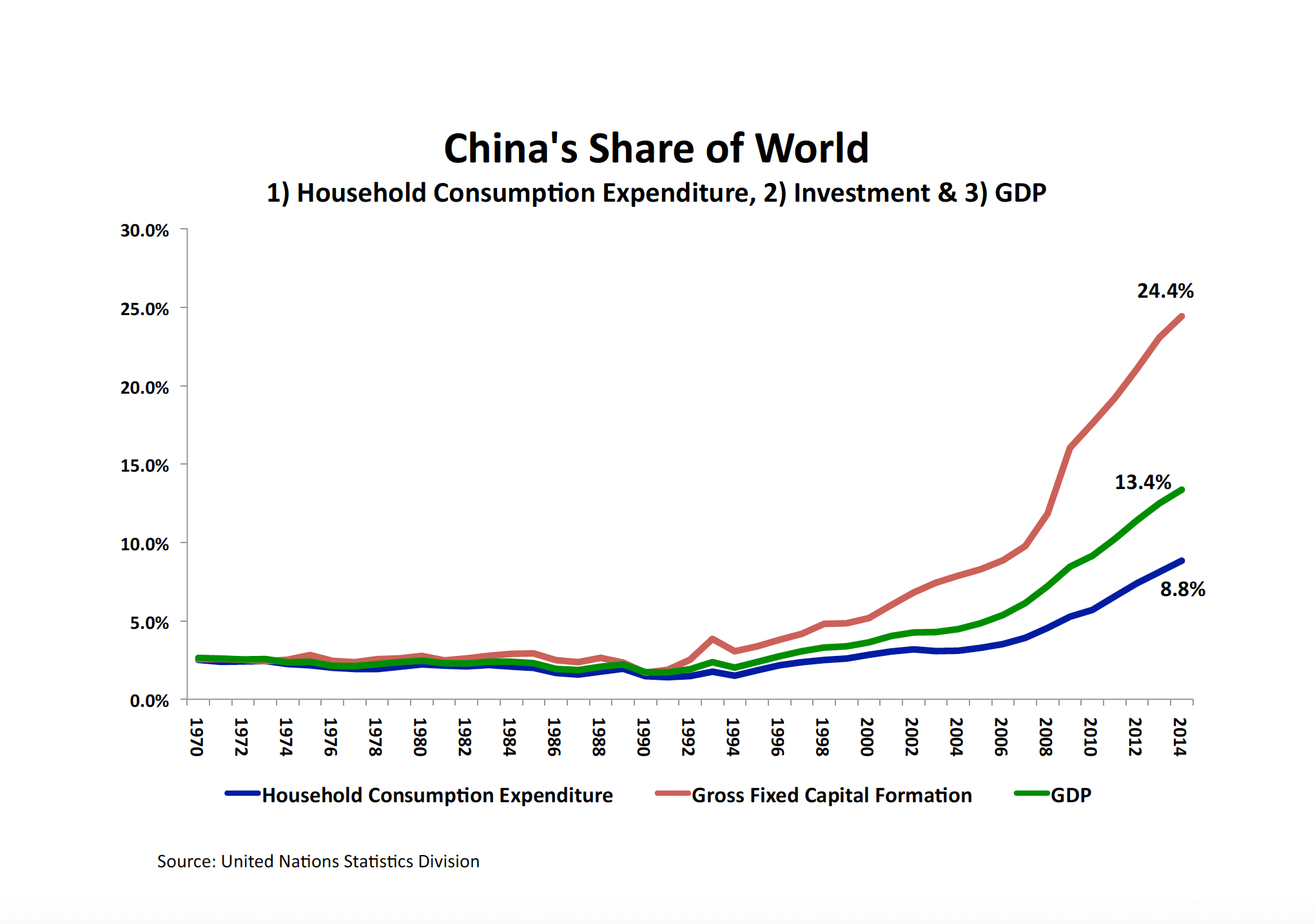

What that means is that China produces far more than it consumes. In the past, China was able to export its surplus production to the rest of the world. Now, however, the global economy is too weak to continue absorbing more and more Chinese exports every year. Moreover, the world is already saturated with Chinese goods. The following chart clearly illustrates the problem.

China’s economy (GDP) makes up 13.4% of the entire world economy (as shown in the green line). However, Chinese Household Consumption Expenditure (in blue) accounts for only 8.8% of the world total for Household Consumption. Chinese Investment (in red), on the other hand, makes up practically a quarter (24.4%) of all the Investment in the world.

Furthermore, China’s share of world investment has been growing rapidly. Between 2000 and 2014, China’s Investment grew at an annual average rate of 16.5% a year vs. only 5.5% average Investment growth for the world as a whole. If those growth rates were to persist for the next ten years, China’s Investment would make up 64% of all the Investment in the world by 2025.

Such a high share of global Investment by China is not going to be possible, either economically or politically. Trade tensions are rising dramatically. The political backlash against free trade and against the negative consequences of Globalization is threatening to overthrow the pro-free market political establishment in the United States and across Europe. China is not going to be allowed to continue selling ever-increasing amounts of its excess production to the rest of the world.

Chinese policymakers have said they will change China’s economic growth model so that going forward the economy will be driven by Consumption instead of Investment. But that won’t be possible. Consumption has increased in China because INVESTMENT has created hundreds of millions of jobs. If China now begins to close down factories and mines in industries where there is excess capacity (i.e. nearly every industry), then jobs will be lost and Consumption will decline. Those losing their factory jobs may find work in the “services industry”, but, as the experience of the US demonstrates, service sector jobs pay less than factory jobs. So, if China reduces Investment, Consumption will fall too.

In short, the income of the 7 billion people on earth is not enough to absorb current global production. It hasn’t been for the last 20 years or more. But, increased borrowing (indebtedness) enabled people to continue buying more even as their incomes stagnated.

That boom ended in 2008. Now the world is left with tremendous excess capacity. Income growth and the growth in indebtedness are too weak in the US (and Europe) to drive the global economy. Consequently, the global economy is too weak to absorb more Chinese exports every year. In China, per capita income is far too low to allow the Chinese to buy all the goods that China produces. Much of China’s existing industrial capacity is already loss making. Additional Investment will only exacerbate the glut and the losses. Therefore, the slowdown in Chinese Investment and Consumption is almost certain to continue. That slowdown will weigh heavily on the global economy.

Continuing very weak global growth is likely to inflame public discontent in the US and Europe and possibly lead to dangerous political outcomes. The growing backlash against free trade could lead to protectionism and the partial reversal of Globalization. In that scenario the chances of a global Depression would increase significantly.

To prevent that outcome, the world’s policymakers are likely to launch a large-scale, globally coordinated fiscal stimulus program after the next US president takes office in January 2017. If they fail to act, our global recession could become a global depression by 2018.

I have just produced a four video series on China’s Hard Landing for Macro Watch. So, if you would like to learn more about how the economic crisis in China is likely to impact the rest of the world and what that could mean for you, please subscribe to my video-newsletter:

http://www.richardduncaneconomics.com/product/macro-watch/

For a 50% subscription discount, hit the orange “Sign Up Now” tab and, when prompted, use the coupon code: richdad

You will find more than 25 hours of video content available to begin watching immediately. A new video will be added approximately every two weeks.

Original publish date:

June 15, 2016