Blog |

My Warning To Some Of The World’s Largest Investment Managers

February 15, 2017

At the beginning of February I was taken on a roadshow by CLSA to meet with institutional investors in New York, Boston, San Francisco and Los Angeles. I made presentations to roughly two dozen investment firms. Collectively they manage well over US$100 billion. The title of my presentation was "Trump's Recipe For Disaster". In my blog today, I am going to use one chart from that presentation to help explain my concerns about President Trump's proposed economic policies. It shows the United States Balance Of Payments from 1960 to 2015.

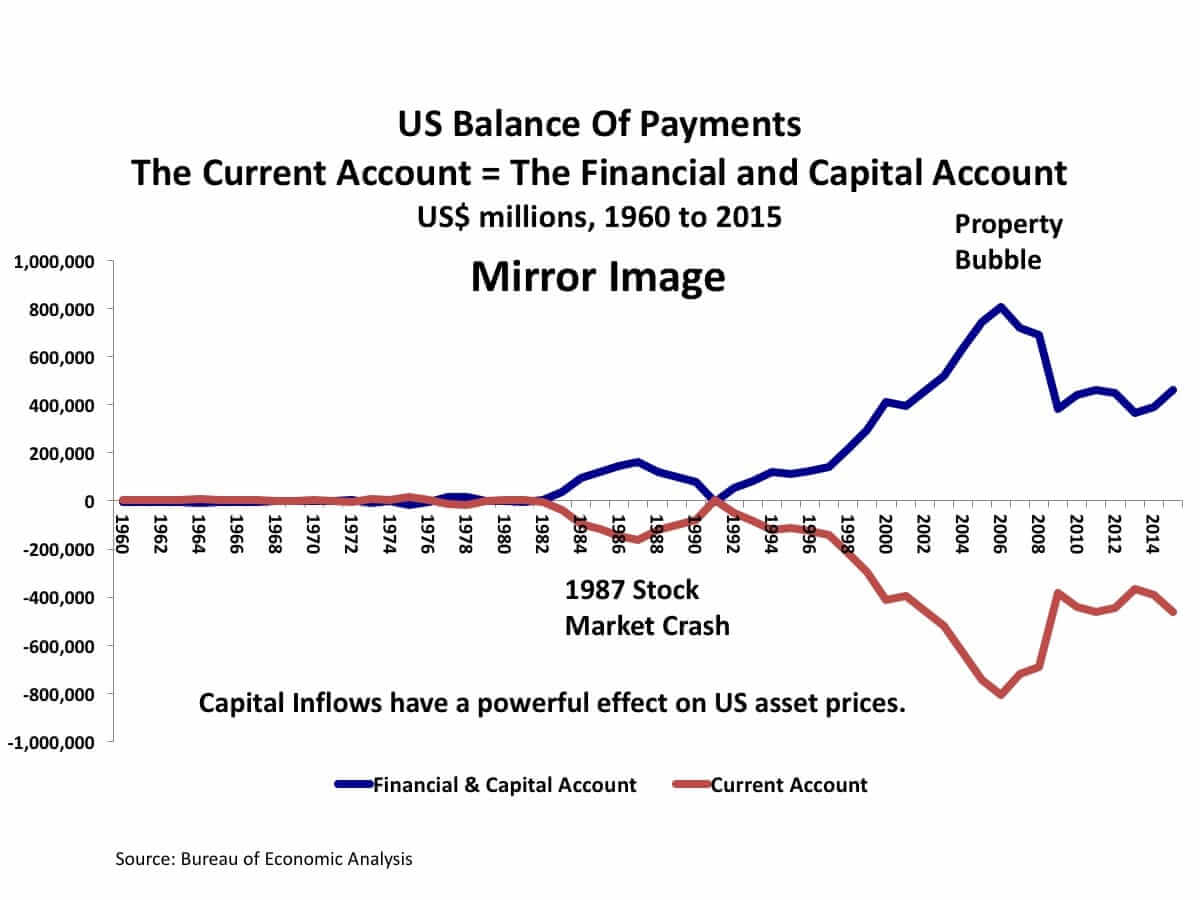

The Current Account = The Financial and Capital Account

The negative (red) line shows the United States Current Account deficit, which is comprised primarily of the country's trade deficit. The positive (blue) line shows the surplus on the country's Financial and Capital Accounts or, in other words, the capital inflows coming into the United States. Notice they are the mirror image of one another. That is because every country's balance of payments has to balance - just like every family's finances have to balance. If a family spends more than it earns, then it has to borrow to finance the gap. It's the same with the US. When it buys more goods from abroad than it sells, then it has to borrow money from abroad to pay for its trade deficit. That means the bigger the US trade deficit becomes, the more capital flows into the United States to finance that deficit.

OK. So let's begin by looking back at the 1960s. Back then the world economy operated under the Bretton Woods International Monetary System; and, under that system, trade between nations had to balance. (You can see that the United States did not begin running large Current Account deficits until the early 1980s, roughly 10 years after the Bretton Woods System broke down.) Consequently, international trade was on a much smaller scale than it is today and the US economy was much more of a closed domestic economy than it is now when Americans buy so much of what they consume from abroad.

In that environment, when President Johnson and then President Nixon began running larger than normal government budget deficits to pay for the Vietnam War overseas and expanded social services at home, those deficits over stimulated the US economy and quickly led to full capacity utilization in the manufacturing sector and to full employment. Prices and wages began to rise sharply and before long the annual inflation rate was well over 10%.

Inflation was alarmingly high throughout most of the 1970s. Finally, in 1981, Fed Chairman Paul Volcker crushed inflation by hiking short-term US interest rates to nearly 20%. That caused a deep recession and 10% unemployment, but the inflation rate came back under control.

At the end of 1980, Ronald Reagan was elected President. He cut taxes and increased government spending on the military, resulting in budget deficits that were much larger than those run by Presidents Johnson and Nixon. President Reagan's budget deficits were the largest peacetime deficits the US had ever experienced. They provided an extraordinary dose of fiscal stimulus to the economy and produced very solid rates of economic growth during the rest of the decade.

However, those deficits did not cause inflation as the deficits of the 1960s and 1970s had. Why not? Because (as you can see in the chart) the United States started running very large trade deficits for the first time ever. By the mid-1980s, the Current Account deficit was 3.5% of US GDP. By buying things from abroad, the United States was able to circumvent the domestic bottlenecks in industrial capacity and labor that had previously led to high rates of inflation.

Fast forward to today. President Trump has pledged to cut taxes, increase government spending on infrastructure and the military and to eliminate the US Current Account deficit. If he does, we will be back in the economic environment that confronted Lyndon Johnson. The tax cuts and increased government spending will over stimulate the US economy, while the elimination of the Current Account deficit would mean that the country would quickly hit full industrial capacity and full employment.

The result would be a rapid return to double-digit inflation. High rates of inflation would push up interest rates, causing credit to contract and crushing the highly leveraged US economy. Asset prices would collapse and the United States and the world would promptly plunge back into a 2008-stlye recession - or worse. The Trump Administration needs to rethink its economic policies. They are a recipe for disaster.

To learn more about how President Trump's economic policies will impact you and your investments, subscribe to my video-newsletter, Macro Watch:

http://www.richardduncaneconomics.com/product/macro-watch/

For a 50% subscription discount, hit the orange "Sign Up Now" tab and, when prompted, use the coupon code:

richdad

More than 32 hours of Macro Watch videos are available to watch immediately. A new video will be added approximately every two weeks.

Original publish date:

February 15, 2017