Blog | Personal Finance

How to Make Money as a Teen

Forget the status-quo lessons and teach your teens something that will really change their financial lives

Rich Dad Personal Finance Team

August 13, 2024

Summary

-

The school system won’t teach your kids what they need to know about money

-

Teach your kids how to make money as a teen so they can be financially free

-

Be wary of tips that keep your kids in the rat race

There’s no shortage of financial ignorance in this world. And most of it starts with the lessons that kids are taught about money from a young age.

Many parents teach their kids nothing. They expect the schools to take care of that for them, perhaps because they don’t know much about it or for some reason they don’t think it’s proper to talk with their kids about money.

Those parents that do teach their kids about money often teach them very basic and sometimes even useless information. Take these five lessons that Christine Burke, writing for the website Lifehacker, thinks are essential for teens to know.

Of all these lessons, only one is remotely related to actual money and how it works and the rest are related to how to spend money. They are mechanics around money but not lessons on money.

The rich teach their kids and teens how to make money without a job

If you were to ask the rich to classify the lessons that Burke suggests that parents teach teens, they would say they are poor-mindset money lessons. These are the types of things the poor and the middle class teach their kids about money.

The rich, on the other hand, teach their kids different money lessons. These lessons are centered on how money works and how to make money work for you. That is, how to make money without a job. Because of this, the rich kids keep getting richer.

A while back, Robert Kiyosaki wrote about how rich dad taught both him and rich dad’s son lessons on money that led them to use what many would consider garbage to make $40 a month together running a comic book library for only a couple hours of day. That was a lot of money in the 1960s. It’s a great example of how rich kids (and those taught by the rich) think about money and how to make it on a different level.

Many think this isn’t fair. In fact, it is often the cry of the poor and the middle class that rich kids are only rich because their parents were rich. That’s actually true a lot of the time. But it has less to do with the money their parents had (though that helps too) and more to do with the lessons that these kids learn about money, both directly and through observation. The rich do have an advantage—the good news is you can use the same advantage to teach your kids about money…just like rich dad taught Robert.

How to make money as a teen

Here are five lessons that will actually be worth teaching your teens about money. And if you’re a teen reading this article, put these lessons to work for yourself as well. Maybe even teach your parents something!

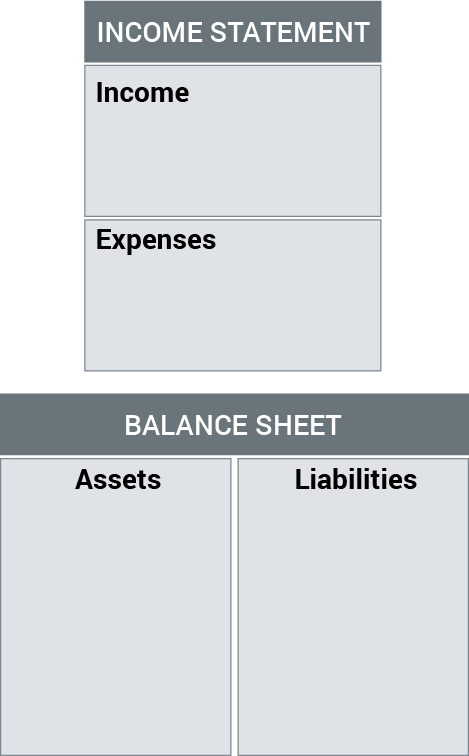

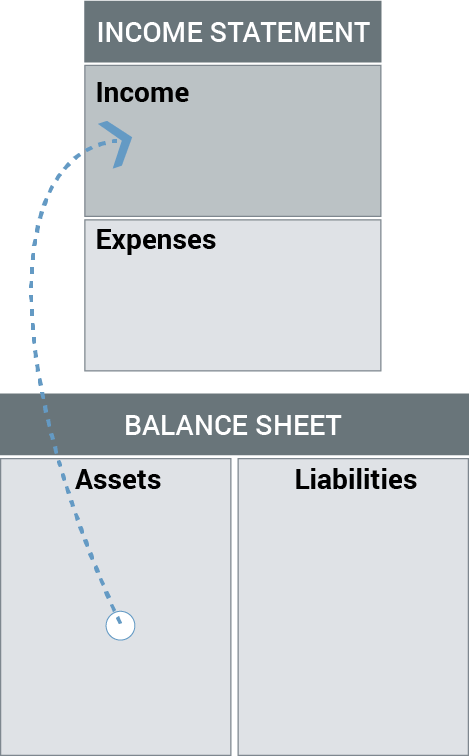

Teen money lesson #1: How to read a financial statement

Basic accounting is all fine and good, but it won’t matter if you can balance a checkbook or update a savings ledger if you don’t know how money flows in and out of your life.

A financial statement is often an intimidating thing, but at Rich Dad, it’s been made as simple as possible. There are four quadrants: income, expenses, assets and liabilities.

The key is to teach your teens the interplay between these quadrants. Simply put, assets, things like investments, real estate, business, etc., allow you to create income:

Liabilities, things like vacations, eating out, a new car, etc., take money out of your pocket:

If your teen understands that they should have more assets bringing in more income than liabilities taking money away via expenses, they will be lightyears ahead of most people, including adults. To learn more on this, read the article, “The Financial Statement Foundation for Being Rich.”

Teen money lesson #2: The difference between an asset and a liability

The key to understanding a financial statement, is to also understand the difference between an asset and a liability. Rich Dad also made this much simpler than most people do in the financial industry.

Simply put, an asset is anything that puts money into your pocket. A liability is anything that takes money out of your pocket.

This actually creates some counterintuitive thinking. For instance, Robert has said for many years, “Your house is not an asset.” People howled and moaned at this, but they didn’t when the housing market crashed. Most people found their houses to be liabilities at the end of the day. Why? They had overpaid and the market made them up-side down. The reality is that real estate, housing included, is only an asset when it puts money in your pocket.

This also helps you understand some really obvious things. Like a tip, pulling money from an ATM, and writing a check almost always means spending money on a liability. How will that money be replaced? If you’re a financially-smart teen, you’ll know the best way to pay for liabilities with passive income from assets.

Teen money lesson #3: How to create money out of thin air

Funny enough, Burke writes that in teaching her child how to write a check, they were surprised to find the money disappeared from their account. “When my son first learned how to write a check, he was astonished to learn that the money magically disappeared from his account and that he’d have to adjust his spending habits to account for the money spent.” It was almost as if the money disappeared out of thin air.

At Rich Dad, we like to also do an equally amazing but opposite magic trick: making money out of thin air.

Teens should know there are two ways to make money in this world: earned or passive.

Earned income is what employees make by exchanging their time for a paycheck. It is the highest taxed income, has the least security, and is capped (you can only work so long and there are only so many hours in the day).

Passive income is what investors and entrepreneurs make. By finding cash-flowing investments or creating and selling a product, they make money even while they are sleeping. It is like money out of thin air. And they can use that money to make even more money by finding more investments or funding new products. It is the least taxed, has the most security because you are in control, and has no cap.

A good example of making money out of thin air is Gabrielle Goodwin. She is someone who knows how to make money as a teen online with her business, GaBBY Bows. You can read more about her in the post “Work Smarter, Not Harder.” Her barrette product sells across the US both in stores and online, including a national distribution deal with Target. She’s twelve, and learning only how to give a tip and write a check would not have allowed her to do what she’s doing today. She understands how money actually works…and how to make it out of thin air.

Teen money lesson #4: How your money gets stolen (legally)

You could teach a teen how to take money out of an ATM, or you could teach them how their money gets stolen, legally, by the government and banks.

There are four wealth-stealing forces when it comes to money: taxes, debt, inflation, and retirement.

The government uses taxes to take your money legally. The banks use credit cards to get you in debt. The Central Banks use inflation to lower the value of the money you do have. And the banking industry uses mutual funds and 401(k)s to steal from you via fees under the guise of saving for retirement.

If teens understood the ways in which their money was stolen legally, they would be able to hold onto more of it and take control of their financial future.

Teen money lesson #5: How to find good people

Rather than teach your kids how to pay people back for liabilities like a night out or one-too-many drinks, teach them how to find great partners for investing and business. Then they can pay them back in the form of profits and dividends. They’ll all get richer together and then no one will really care about who bought the last round.

Teach them the idea of Other People’s Money, aka OPM.

There’s nothing like leveraging OPM to get assets that produce cash flow month in and month out. The reality is if you have a great idea or investment, finding money is easy to do. Not having enough money is never a good excuse.

Teach your kids how to make money as a teen - the right way

So the next time you come across an article about financially educating your children, be sure the tips aren’t contributing to a life in the rat race. Teach them to be financially intelligent, and financially free.

Original publish date:

November 27, 2018