Blog | Personal Finance

The Four Foundations of Financial Literacy

August 06, 2019

The four foundations you need to increase your financial literacy and get richer

This just in: consumer debt, not counting mortgages, is the highest it has ever been, even adjusted for inflation.

According to a depressing article in the “Wall Street Journal” entitled, “Families Go Deep in Debt to Stay in the Middle Class,” consumer debt has risen to over $4 trillion. The mega-rise in debt is filed by:

- $1.5 trillion in student loan debt

- $1.3 trillion in auto loan debt (up 40% when adjusted for inflation over the last decade), at an average of $32,187 per loan

- A surge in unsecured personal loans

As the article points out some could view this rise in debt as a vote of confidence in the future of the economy: “In one sense, the growing consumer debt is a vote of confidence in the future. People borrowing money today expect to have the income tomorrow to pay it back. Consumer debt tends to rise when borrowers feel secure in their jobs.”

However, the rise in costs for basic living expenses would point otherwise. While middle class incomes have gone up 135% over three decades through 2017, unadjusted for inflation, the following basic living expenses have gone up significantly more:

- College tuition by 549%

- Health care by 276%

- Housing costs by 188%

In short, it’s getting more and more expensive to stay in the middle class and more of the middle class are getting poorer and poorer as a result. Meanwhile, the rich in America are getting richer and richer. Why?

How financial literacy can make your rich or poor

According to the “Wall Street Journal” article, “The median net worth of households in the middle 20% of income rose 4% in inflation-adjusted terms to $81,900 between 1989 and 2016, the latest available data. For households in the top 20%, median net worth more than doubled to $811,860. And for the top 1%, the increase was 178% to $11,206,000.”

What does this mean?

It means that, as I mentioned earlier, the middle class are getting poorer and poorer why the rich are getting richer and richer. A big catalyst for this is the difference between the financial literacy of the middle class and that of the upper class.

In 2017, Champlain College released the results of its study looking at the state of financial literacy in the US (by state, in fact). The study’s methodology looked at, in some cases, 71 different data points in five categories: financial knowledge, credit, savings and spending, retirement readiness and other spending, and protect and insure.

The results? Not good.

As Vermontbiz.com reports, the study “shows that more than three-quarters of adults live in states with poor grades. This means that too many American adults are deficient in financial knowledge and skills, which leads them to make uninformed and often poor decisions about their money…The number of financial decisions an American citizen has to make continues to increase, and the variety and complexity of financial products continue to grow. Adults often do not fully understand debit and credit cards, mortgages, banking, investment and insurance products and services, retire-ment planning, and many other financial topics.”

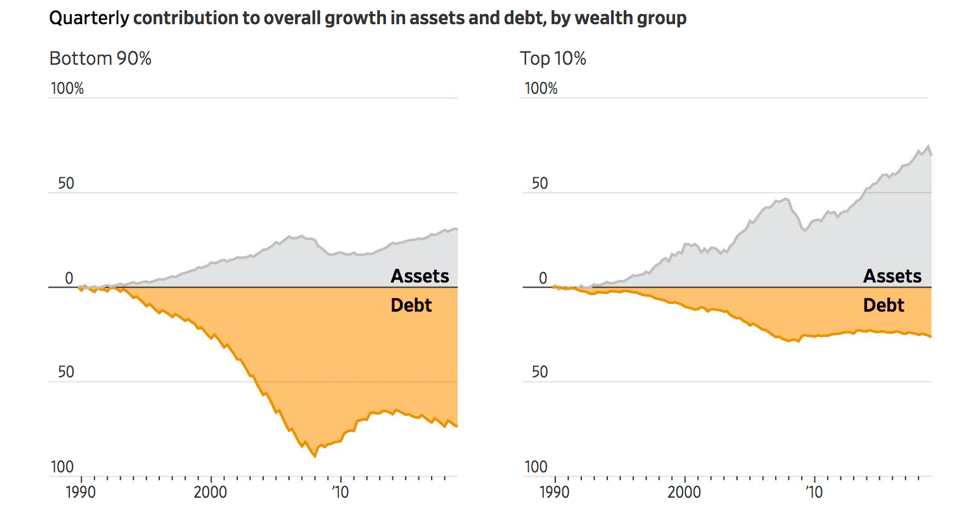

The gap in financial literacy between the middle class and the rich can be easily seen in this graphic from “The Wall Street Journal” article:

Simply put the lack of financial literacy has caused the middle class to increase their debt nearly three times more than their assets. The rich, on the other hand, have the inverse ratio. They have increased their assets by nearly three times their debt. In all likelihood the rich are using that debt to fund the acquisition of their assets, while the middle class are leveraging their assets to get into deeper debt for liabilities. The most basic of financial equations for getting poorer.

The cost of poor financial literacy

In another interesting, though much less informal survey, The Financial Educator’s Council asked 3,006 people this question: “Across your entire lifetime, about how much money do you think you have lost because you lacked knowledge about personal finances?”

As CardTrack.com reports, the of lack financial knowledge is collectively costing Americans more than $2.3 trillion dollars over their lifetime. “Respondents estimated that their lack of financial knowledge cost them an average of $9,724.83 (calculated by averaging the total number of respondents choosing each category, using the lowest number in each spread).”

Personally, I’d say these folks are low-balling. After all, how can you expect people with no financial knowledge to accurately guess how much that lack of knowledge is truly costing them? As they say, “You don’t know what you don’t know.”

At Rich Dad, we’ve seen folks grow their financial knowledge to make more in a month in passive income than the respondents estimated lifetime loss. Indeed, a little bit of financial education put into practice goes a long, long way—and so does a lack of financial education.

How do you fix poor financial literacy?

Many people have opinions on how to fix the problem of poor financial literacy. Unfortunately, much of what is labeled out there as financial education leaves a lot to be desired. From my experience, it centers on concepts like saving, investing in a 401(k), getting a college degree, paying down debt, and home ownership. In short, it centers on the old ideas about money.

I’ve said it before, when you follow the old rules of money, you’re screwed financially.

So, given the huge costs of financial illiteracy, and the lack of true financial education in America, I thought I’d briefly offer what should be the four foundations of financial literacy.

These four foundations are the baseline for a truly comprehensive financial education.

Financial literacy foundation #1 - The difference between an asset and a liability

Many people think they know what is an asset. For instance, you probably think your house is an asset—but it’s not. The truth is that just as there are two definitions of an asset.

Accountants use one definition that requires lots of financial calisthenics to make people and companies feel richer than they really are. This keeps them employed and their clients blissfully ignorant.

The rich use another definition grounded in simplicity and reality. An asset is anything that puts money in your pocket and a liability is anything that takes money out of your pocket.

Your house is not an asset because it takes money out of your pocket each month. Even if you own your house outright, you still have to pay for the taxes, maintenance, and more out of your own pocket. This is why it’s not hard to see that the middle class struggling to buy a house, even as the price of housing has outpaced their earnings, has made them poorer, not richer.

Conversely, if you own a rental property, that can be an asset—if it puts money in your pocket each month in the form of cash flow. When your tenant pays rent, they cover your mortgage, maintenance, taxes, and more. This would explain why the rich, the top 10%, can increase their debt but exponentially increase their assets. They use debt to buy assets that create more wealth.

Financial literacy foundation #2 - Cash flow versus capital gains

Most people invest for capital gains. The rich invest for cash flow.

Simply put, investing for capital gains is like gambling. You invest your money and hope the price goes up. For instance, many people buy a house hoping they’ll be able to sell it for more money later. In the meantime, they have to pay their mortgage and home expenses. Money goes out of their pocket. It becomes a liability.

The problem is that when you invest for capital gains you have no control over whether the price goes up or down, and the bigger issue is, if you do make a profit, you pay the highest rate in taxes.

Conversely, the rich invest for cash flow. So, for instance, they buy investment real estate with other people’s money, find tenants to pay the expenses, and collect rent each month. It becomes an asset. And if there’s capital gains, that’s a bonus.

By investing for cash flow instead of capital gains, the rich have control over their income and pay the lowest rate in taxes—and sometimes nothing in taxes.

But investing for cash flow, while a simple concept, requires a strong financial education in order to make your own financial decisions.

Financial literacy foundation #3 - Using debt and taxes to get richer

Your financial adviser will tell you that debt is bad and taxes are inevitable. But the rich understand that both debt and taxes can be used to create immense wealth.

When it comes to debt, there are two kinds—bad and good. When your financial adviser tells you to stay out of debt, she means stay out of bad debt.

Bad debt comes in the form of borrowing money for liabilities such as using credit cards to buy TVs and take vacations, borrowing a line of credit on your personal home, and more.

Staying out of bad debt is good advice, but the problem is that your financial adviser won’t tell you about good debt.

Good debt is debt used to purchase assets like rental property.

When you use the bank’s money to purchase cash-flowing real estate, you use less of your own money to secure an asset by paying only a down payment instead of full price, and your tenant’s rent pays off your debt while you own the asset and pocket the profit.

When it comes to taxes, the rich understand that governments write tax codes to encourage specific types of behavior. If governments want you to build affordable housing, they give you a tax cut. If they want to encourage oil exploration, they give you a tax cut. If they want to see higher employment, they give you a tax cut.

The secret is that most tax benefits are made to help entrepreneurs and investors. With the right financial education, you too can utilize the tax code to not only get richer, but also pay nothing in taxes.

Utilizing good debt and getting richer through taxes takes a high level of financial literacy. But everyone can learn and put these principles into practices.

Foundation literacy foundation #4 - Making your own financial decisions

When you’re not confident about your knowledge of money, you let others make your financial decisions for you.

You let your broker decide how your money should be invested. You let your bank tell you what interest rate is worthy of your money. You follow whatever investing trend is popular in the news.

Do you want a better life for you and your family?

Stop struggling. Take our short quiz and discover how to create a life of freedom.

Take The Quiz Now

Take The Quiz Now

The rich don’t follow the crowds. They set the trends and are gone by the time the trends become mainstream. What’s their secret? They think for themselves about money and make their own financial decisions because they have a high financial intelligence.

The key to building great wealth is having great knowledge to act on and great wisdom to know which course of action is the best.

This kind of knowledge and wisdom only comes through a high financial intelligence gained from applying yourself to financial education.

Are you ready to increase your confidence about money by increasing your financial education? Are you ready to start making your own financial decisions?

Check out our free, financial education community here, and start your journey to financial literacy today.

Original publish date:

April 03, 2017