Why “all debt is bad” is outdated adviceHow the poor use debt

A well-known school of personal finance, popularized by debt-avoidance advocates, argues that nearly everything should be purchased with cash and that debt of any kind should be eliminated as fast as possible. It’s not unreasonable advice for someone drowning in high-interest consumer debt — but as a universal rule, it misses the point entirely.

Debt is not incidental to the American economy; it’s foundational to it. The financial system runs on steady credit expansion, and without borrowing — of any kind — commerce as we know it would seize up. The real question isn’t whether to use debt. It’s which kind of debt to use, and for what.

Unfortunately, the way most people use debt and the way sophisticated investors use it are almost opposite strategies.

What is bad debt? Common examples and why it’s so expensive

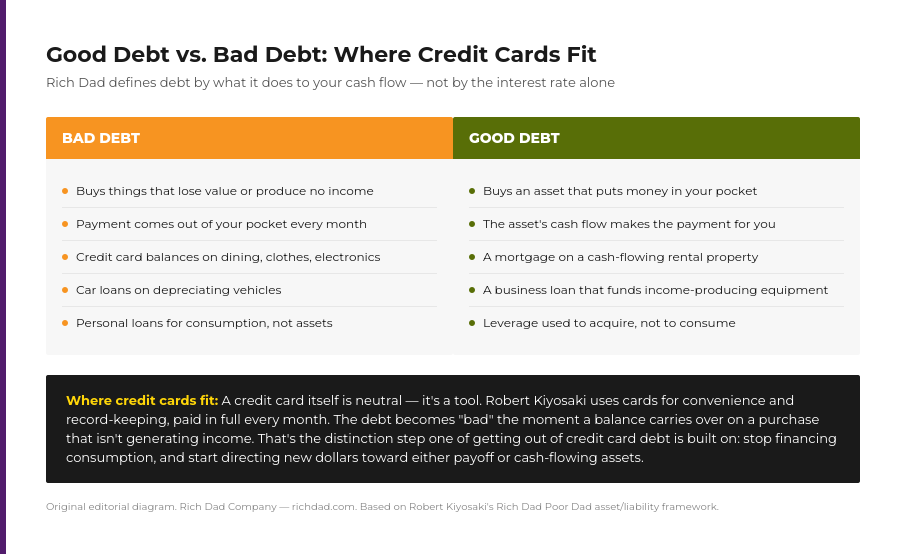

Bad debt is generally used to buy things that lose value the moment you own them, and it rarely — if ever — generates the income needed to pay for itself.

High-interest credit cards

As of mid-2026, the average credit card interest rate sits close to 19.6% according to Bankrate, while new card offers average nearly 23.8% APR according to LendingTree — and borrowers with fair or poor credit routinely see rates above 27%. Beyond the headline rate, cards often carry hidden costs: late fees, annual fees, and foreign transaction charges that quietly add up.

Credit cards are not inherently good or bad. It’s how they’re used. The trouble is that most people use them to finance things that are consumed or that depreciate — clothes, electronics, travel — while making only minimum payments. That combination is brutal: substantial interest paid over years, for purchases that have long since lost their value.

Loans for liabilities

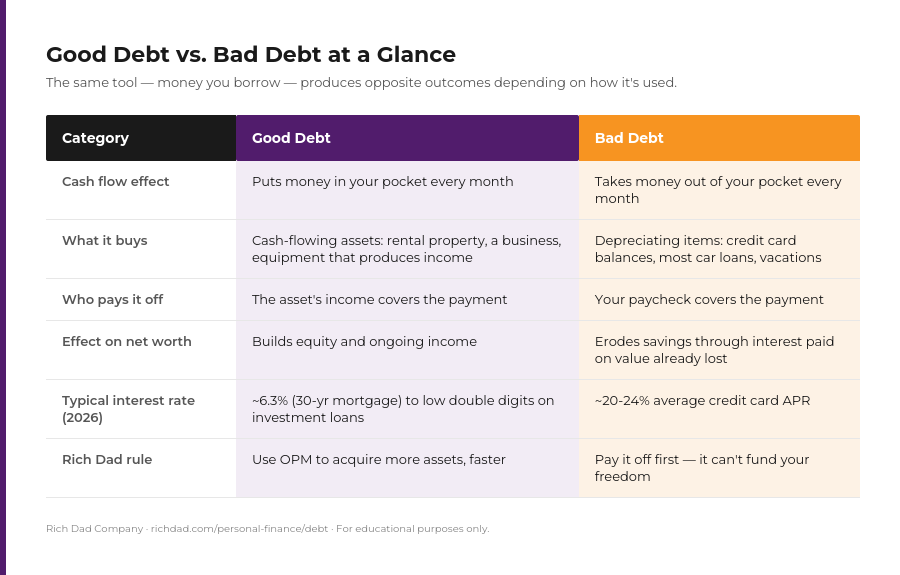

Car loans, personal loans, and payday loans all fall into this category more often than not. Even a mortgage on a personal residence belongs here because a home you live in doesn’t put money in your pocket. It takes money out, every month, in the form of a payment, taxes, insurance, and upkeep. That’s not an argument against ever buying a home; it’s an argument against calling it an investment.

This pattern of using bad debt to acquire depreciating assets is what keeps most households financially treading water for decades. Working through what that actually costs makes the case clearly:

A $5,000 credit card balance at a representative 20% APR, paid down with minimum payments only, takes roughly 23 years to pay off and costs about $7,723 in interest — more than the original balance itself — according to Bankrate’s own repayment calculator. That’s the mechanics of bad debt in a single example: money leaving your pocket, for years, for a purchase that likely stopped mattering long ago.

What is good debt? The cash flow test

Good debt is the type sophisticated investors use to grow net worth — by borrowing to acquire cash-flowing assets using Other People’s Money (OPM), both the bank’s and outside investors’.

OPM is a foundational Rich Dad concept and a hallmark of financial intelligence. Used well, good debt and OPM can dramatically increase return on investment — and in the right structure, produce what Rich Dad calls an infinite return, where none of an investor’s own capital remains in the deal.

Error: Campaign not found.

The simplest way to evaluate any debt is the cash flow test: does the income the asset produces cover the loan payment, with money left over? If yes, it’s a candidate for good debt. If the answer is no — or if there’s no income at all, just the hope of future appreciation — it’s speculation, not investing.

The downside of debt financing is that lenders will typically only cover a portion of a purchase price — commonly 70% to 80% for investment real estate. That leaves a choice: fund the rest with your own capital, or bring in other people’s money. Structured well, the more of a deal financed with OPM, the higher the return on the capital an investor does put in.

This isn’t a fantasy reserved for the already-wealthy. Rich Dad real estate advisor Ken McElroy built his company, MC Companies, by finding good deals, doing the diligence, negotiating with lenders and sellers, and managing the resulting properties — while investors lined up to fund the purchases. He started small and worked up to the large multifamily deals he does today. The formula is the same at any scale.

How much debt are Americans actually carrying?

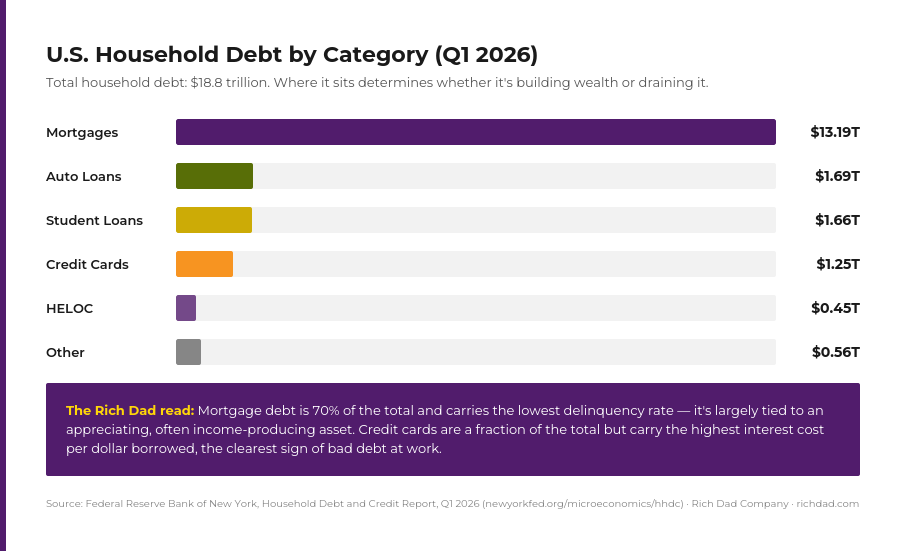

Total U.S. household debt reached a record $18.8 trillion in the first quarter of 2026, according to the Federal Reserve Bank of New York — up more than 32% from pre-pandemic levels.

Mortgage debt makes up roughly 70% of that total and carries the lowest delinquency rate of any category, largely because it’s secured by an asset that, historically, appreciates. Credit card debt is a much smaller slice of the pie — about $1.25 trillion — but it carries by far the highest interest cost per dollar borrowed, which is exactly why it does the most damage to household cash flow relative to its size.

The pattern holds up nationally: the debt category tied to an appreciating, often income-producing asset is the safest and cheapest to carry. The debt category tied to consumption is the most expensive and least forgiving.

How the rich multiply returns with good debt and OPM

Here’s a simplified version of the math Rich Dad has taught for years, updated for today’s borrowing environment.

Say “Jane” has $100,000 to invest, and she’s found a solid rental market where $100,000 properties rent for about $900 a month — the kind of deal a diligent investor can still find. She has two paths.

Path one: use her own money

Jane buys five $100,000 properties, putting 20% down on each ($20,000 x 5 = $100,000) and financing the rest with a bank loan. At today’s rates — 30-year fixed mortgages are running close to 6.3%, per Freddie Mac — her all-in payment (principal, interest, taxes, and insurance) runs about $655 a month per property. That leaves $245 a month in cash flow per property, or $1,225 a month total — about $14,700 a year, a roughly 14.7% return on her $100,000.

Path two: add OPM

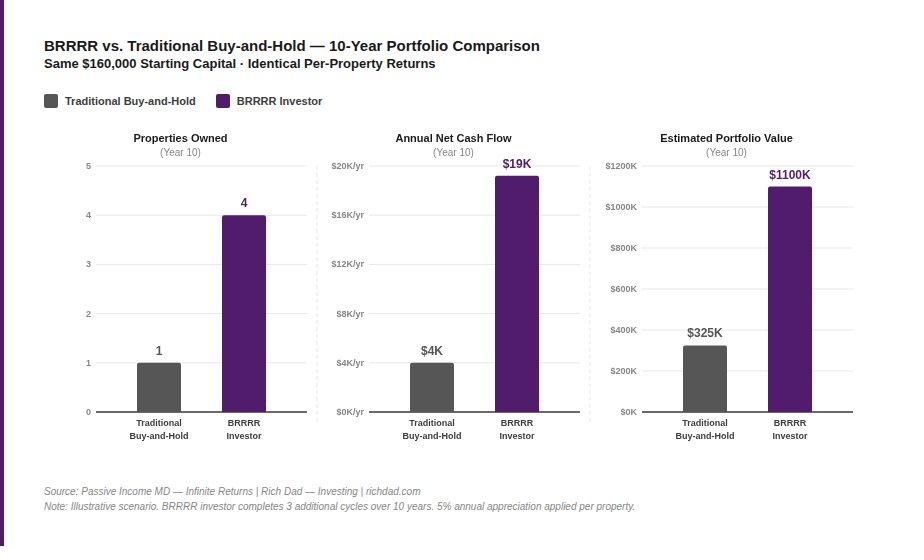

Instead of putting 20% down on five properties, Jane uses her $100,000 to put just 5% down on twenty properties, bringing in outside investors to cover the remaining 15% needed on each deal. The bank still finances 80% at the same terms (about $655 a month in debt service), and Jane pays her OPM investors around 8% on their contribution — roughly $100 a month per property. Total monthly cost per property: about $755. Cash flow per property: about $145 a month.

Multiply that across 20 properties and Jane collects roughly $2,900 a month — about $34,800 a year — on the same $100,000. That’s closer to a 35% return, and she now holds ownership positions in 20 assets instead of five. Later, she can refinance, return investor capital, and keep the cash flow indefinitely: an infinite return.

This is essentially the same principle behind the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat) — recycling the same capital across multiple properties instead of parking it permanently in one deal. Both approaches rely on the same idea: good debt, used well, multiplies what your own capital can accomplish.

How to start using good debt without getting burned

Good debt is a skill, not a shortcut, and it comes with real risk if it’s used carelessly. A few principles keep it on the right side of the line.

Get bad debt under control first. High-interest consumer debt has to be serviced regardless of what else is going on, and it crowds out the capacity to take on productive debt. Rich Dad’s guide to getting out of bad debt walks through the process step by step.

Error: Campaign not found.

Run the cash flow test before signing anything. Does the income the asset produces cover the debt payment, with a margin left over? If the answer depends on the asset appreciating rather than on cash flow it’s already generating, that’s a red flag.

Build financial education before borrowing to invest. Understanding a deal well enough to defend it to a lender — or to an OPM investor — is the whole game. Rich Dad’s real estate investing resources are a starting point.

Start small. Ken McElroy didn’t begin with hundred-unit apartment complexes, and Jane’s twenty-property scenario above didn’t happen overnight. Financial intelligence compounds the same way good debt does — a little at a time, structured well, repeated consistently.

FAQs

Ask whether the asset the debt buys puts money in your pocket every month or takes it out. If the income covers the payment and leaves a surplus, it’s a candidate for good debt. If you’re the one covering the payment out of your paycheck, it’s bad debt.

A personal residence is a liability rather than an asset, because it doesn’t generate income — it costs money every month in payment, taxes, insurance, and upkeep. That doesn’t mean homeownership is a mistake; it means it shouldn’t be counted as an investment.

Only if the resulting income potential clearly justifies the cost. A loan for a credential that meaningfully raises lifetime earnings can behave like good debt; a large loan with no clear return on future income behaves like bad debt regardless of the purpose.

Start with financial education and a small deal you understand well. Investors follow people who can find good opportunities and manage them competently — not the other way around. Track record and financial intelligence attract capital more reliably than having capital in the first place.

Yes. Even cash-flowing debt carries risk — vacancy, rate changes, market shifts — so it should always be sized to what the underlying asset’s income can comfortably support, with a buffer.

Debt, on its own, is neither the villain nor the hero of the story. It’s leverage — and like any tool, its impact depends entirely on what it’s used to build. Get bad debt out of the picture, learn to run the cash flow test on every opportunity, and start putting good debt and OPM to work, even on a small scale. That’s the path from working for money to having money — and other people’s money — work for you.