When Robert Kiyosaki was a young boy, his rich dad (his best friend’s father), told him: “You can make a lot of money and still not be rich.” By this, he meant that you could have high income but also low financial intelligence. Many high earners lose their money to two things, expensive liabilities—like fancy cars, long vacations, McMansions—and taxes.

Back in 2010, Robert wrote about a Fortune Magazine article entitled “Why the ‘rich’ aren’t feeling so rich”. The article covered the term its author had coined, “HENRY,” which stands for “High Earners, Not Rich Yet.” As Robert wrote then, “What Tully is getting at is that those we’d consider rich because they make a lot of money, such as doctors and lawyers making $250,000 to $500,000, aren’t really rich at all.”

HENRY pays the highest

As it stands today, these high-paid employees pay the most in taxes, with effective rates between 33% to 39.6% from roughly $191,000 to $418,000 a year in earned income. And unfortunately for these high-earning employees, there isn’t much they can do to find relief, aside from a mortgage deduction and family credits.

Some people find this to be incredibly unfair. Why should you pay higher taxes simply because you make more money? Depending on where you land on the political spectrum, you’ll most likely have passionate arguments for or against the idea of taxing the rich.

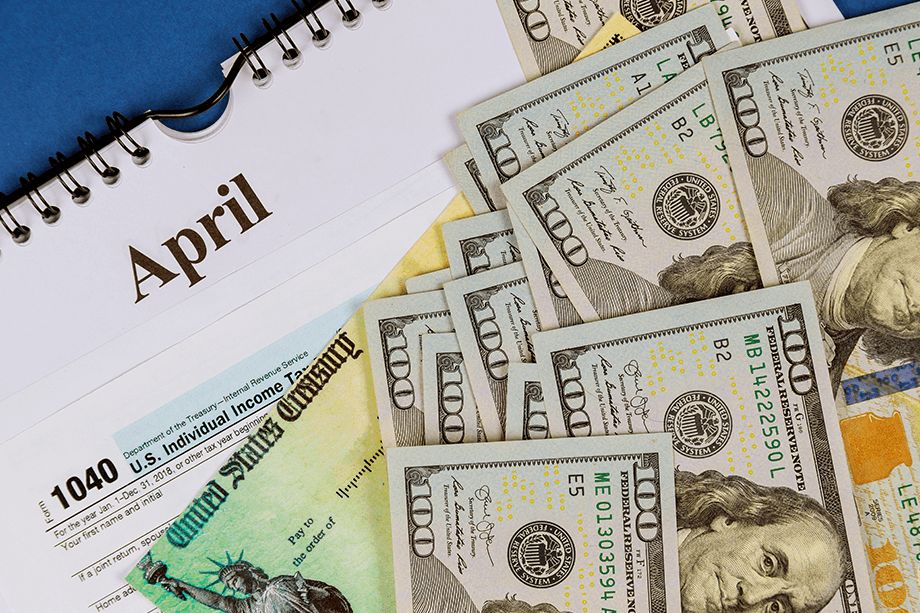

The sure thing of life: taxes

They say there are only two sure things in life: death and taxes. And nobody likes either of them. For now, let’s focus on taxes.

Rich dad also said to Robert, “When it comes to taxes, the rich make the rules…If you want to be rich, you need to play by the rules of the rich.”

The rules of money are skewed in favor of the rich, and against the working and middle classes. After all, someone has to pay taxes.

The middle class, of course, does not like this. That is why they get so mad when they find out that the rich can avoid paying taxes and when they find out that the rich often avoid paying taxes because they help write the rules.

Opportunity zones

A good example of this comes from an article by the publication “Vox” called, “The new hotness for tech billionaires? Do-gooder investments they can write off on their taxes.” The article talks about a tax law called “Opportunity Zones.” Essentially, these are low-income areas of the country where the rich can invest their money to spur economic development. By doing so, they can defer their capital gains taxes through 2026, and they can also pay no taxes on the profit they make from the in-vestments in these opportunity zones.

The article itself, from the title to many of the quotes, is filled with contempt for the idea of rich people saving money on taxes by investing in low-income areas. But per-haps most galling to folks is that the law was crafted by a rich person.

“Behind it all is another Silicon Valley billionaire: Napster founder and early Facebook executive Sean Parker, who is using his celebrity and Rolodex to schmooze the wealthiest people in town. He’s been chatting up people like his longtime friend Peter Thiel, LinkedIn founder Reid Hoffman and venture capitalist John Doerr, pitching them on the idea in the way only a true peer can.”

Again, as rich dad said, “When it comes to taxes, the rich make the rules.”

Why paying $0 in taxes can be a good thing

To piggyback, during the 2016 election cycle, then candidate Donald Trump received a lot of criticism for not releasing his tax returns.

Jumping on this, Hillary Clinton and the Democrats speculated that one reason might be that he paid $0 in taxes. Most people saw this and immediately rose up in righteous anger. That would be so unfair!

Robert, however, was compelled to write a post called, “Why I Hope Donald Trump Paid $0 in Taxes.” in which he defended the fact that Trump may not have paid taxes. As he wrote then:

As you probably know, the tax codes in the US and in many different countries are long and complicated. The question is, why?

The reason is that government leaders learned a long time ago that the tax codes could be used to make people and businesses do what they want by utilizing the tax code.

In short, the many credits and breaks that are found in the tax code are there precisely because the government wants you to take advantage of them. For instance, the government wants cheap housing. Because of this, there are many tax credits for affordable housing that developers and investors can take advantage of that minimize their tax liability, put more money in their pocket, and in turn, create affordable housing. Everyone wins.

There are many scenarios like this in the tax code that incentivize investors and entrepreneurs to do activities the government is looking for while rewarding those who take those actions with lower-or zero-tax burden.

Because of this, limiting your tax liability actually means you’re doing what the government wants you to do through the tax code. And that is the most patriotic thing you can do.

One of the reasons Robert supported Donald Trump as president was because he knew Trump understood how money actually works, including using the tax code to force the right behavior for the country.

Playing the game of money

When it comes to conversations like this, most people appeal to some sense of justice. It’s not fair, they cry, that the rich get to make the rules when it comes to taxes. It’s unjust, they say, that the rich can avoid paying taxes while the middle class and the poor are stuck with the bill.

Sure, it’s not fair. But, let’s face it: life isn’t fair.

Rather than focus on what’s fair and complaining, consider learning the rules the rich make and play by them yourself. Of course, the government is in on this. They, after all, create the tax code to encourage certain behavior that they want people to do, like investing in poor areas. Take Trump, for example.

Playing by the Rules of the Rich

There are many ways that the rich make a lot of money and pay little to no money in taxes, and anyone can use them. As an illustration, here’s a real-life situation in which Robert and his wife, Kim, played by the rules of the rich and minimized their taxes:

- They put $100,000 down to purchase 10 condominiums in Scottsdale, Ariz. The developer paid them $20,000 a year to use these 10 units as sales models. So, they received a 20 percent cash-on-cash return, on which they paid very little in taxes because the income was offset by the depreciation of the building and the furniture used in the models. It looked like they were losing money when they were in fact making money.

- Since the real estate market was so hot, the 380-unit condo project sold out early. Their 10 models were the last to go. They made approximately $100,000 in capital gains per unit. They put the $1 million ($100,000 x 10 units) into a 1031 tax-deferred exchange. They legally paid no taxes on their million dollars of capital gains.

- With that money, they purchased a 350-unit apartment house in Tucson, Ariz. The building was poorly managed and filled with bad tenants who had driven out the good tenants. It also needed repairs. They took out a construction loan and shut the building down, which moved the bad tenants out. Once the rehab was complete, they moved good tenants in and raised the rents.

- With the increased rents, the property was reappraised and they borrowed against their equity, which was about $1.2 million tax-free, because it was a loan—a loan which their new tenants pay for. Even with the loan, the property still pays them approximately $100,000 a year in positive cash flow.

- Kim and Robert then invested the $1.2 million in another 350-unit apartment house in Flagstaff, Ariz., a hot property market, all tax free.

Move Money, Don’t Park It

This is an example of an investment strategy known as the velocity of money. Moving your money makes more sense than parking it in cash, bonds, equities, or mutual funds—the strategy most financial advisors recommend.

The Kiyosakis have several such scenarios active at any one time. They have lots of monthly cash flow, which they reinvest, but rarely have any liquid cash sitting around to be taxed.

In the above example, they started with $100,000 they earned tax-deferred from another investment. The $100,000 eventually allowed them to borrow over $20 million from banks, tax-free. How long would it take you to save $20 million by parking your money somewhere, as most financial advisors recommend?

Chipping Away at Taxes

Clearly, one of the reasons the rich get richer is because they earn a lot of money without paying much, if anything, in taxes. They know how to use banks’ tax-free money to become richer.

On the flip side, the poor and middle-class toil away for their money, pay more in taxes the more they earn, and then park their earnings in savings and/or retirement accounts. In the meantime, they receive little or no cash flow on which to live while wait-ing for retirement—when they’ll live on their meager savings.

Doesn’t it make more sense to play by the rules of the rich, and earn more while paying less in taxes?