“The average person is 95 percent eyes and only five percent mind when they invest,” Robert Kiyosaki writes in Rich Dad Poor Dad. “If you want to become a professional in the B and I quadrants, you need to train your eyes to be only five percent and train your mind to be the other 95 percent.”

That statement carries more weight today than it did when the book was first published. Financial products have grown more complex, markets shift faster, and the gap between those who understand money and those who don’t has never been wider. Understanding what financial intelligence is — and how to build it — may be the single most valuable educational investment a person can make.

What Financial Intelligence Actually Means

The term “financial intelligence” is used loosely in popular culture — often as a synonym for being good with money. But the Rich Dad definition is more precise. Financial intelligence is the mental capacity to understand how money works, recognize where it is flowing, position oneself in its path, and keep it working once it arrives.

This is distinct from simply earning a high income. A physician earning $400,000 per year who loses half to taxes, spends the rest, and retires with no passive income has low financial intelligence. A landlord earning $80,000 in net rental income who pays an effective tax rate of 8 percent and reinvests the difference has high financial intelligence. The difference is not income — it is financial education applied.

Rich Dad’s core premise is that money is invisible to most people. Every day, trillions of dollars move electronically around the globe through banks, markets, and investment vehicles. The problem is not a shortage of money — it is a shortage of the education required to see where it is going and how to access it.

Financial Intelligence vs. Financial Literacy: Why the Difference Matters

Financial literacy and financial intelligence are related but not the same. Financial literacy is the foundation — the ability to understand financial concepts, read a balance sheet, and speak the language of money. Financial intelligence is what you build on top of that foundation: the wisdom to apply literacy in real-world decisions, to see patterns others miss, and to act when others freeze.

Think of it this way: a person who can read a map has geographic literacy. A person who can navigate through a city in a traffic emergency, find shortcuts, and arrive on time has geographic intelligence. The first is prerequisite; the second is the goal.

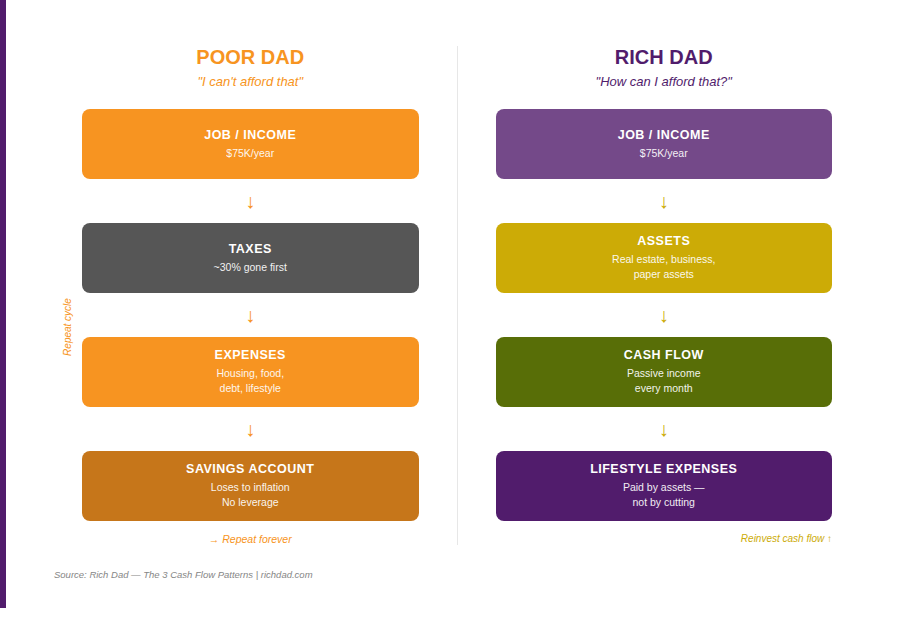

Rich dad taught Robert that financial literacy begins with understanding four words: income, expense, asset, and liability. Most people never truly master these four concepts. They believe their home is an asset, when Rich Dad defines an asset as anything that puts money in your pocket and a liability as anything that takes money out. That single distinction, fully understood and applied, changes every financial decision a person makes.

The financial literacy section of Rich Dad provides foundational resources for building this base. But the goal is always to translate that literacy into intelligence — into action, not just awareness.

Why Most Americans Have a Low Financial IQ — The Data

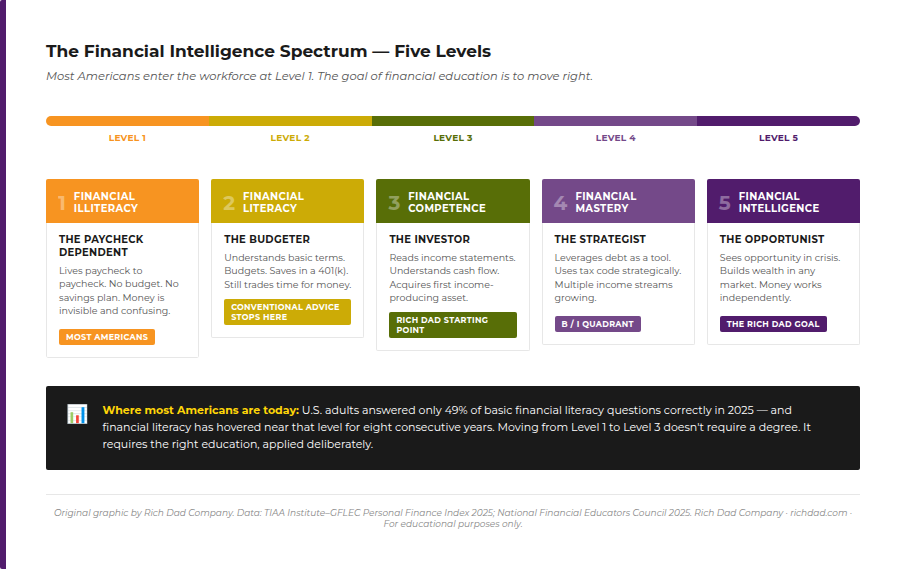

The financial literacy crisis in America is well-documented. According to the 2025 TIAA Institute–GFLEC Personal Finance Index, U.S. adults answered only 49 percent of basic financial literacy questions correctly — a number that has hovered near that level for eight consecutive years despite growing awareness and policy initiatives.

The National Financial Educators Council’s 2025 survey found that poor financial literacy cost the average American $948 over the year, with 14.6 percent of respondents reporting losses exceeding $2,500. Perhaps most striking: more than 80 percent of adults who attended high school wish they had been required to take a personal finance course.

The school system teaches people to be employees — to earn income, pay taxes, spend what remains, and save whatever is left. This is what Rich Dad calls the E-S side of the CASHFLOW® Quadrant. It produces financially competent workers, but not financially intelligent investors. The educational gap is not accidental — it is structural.

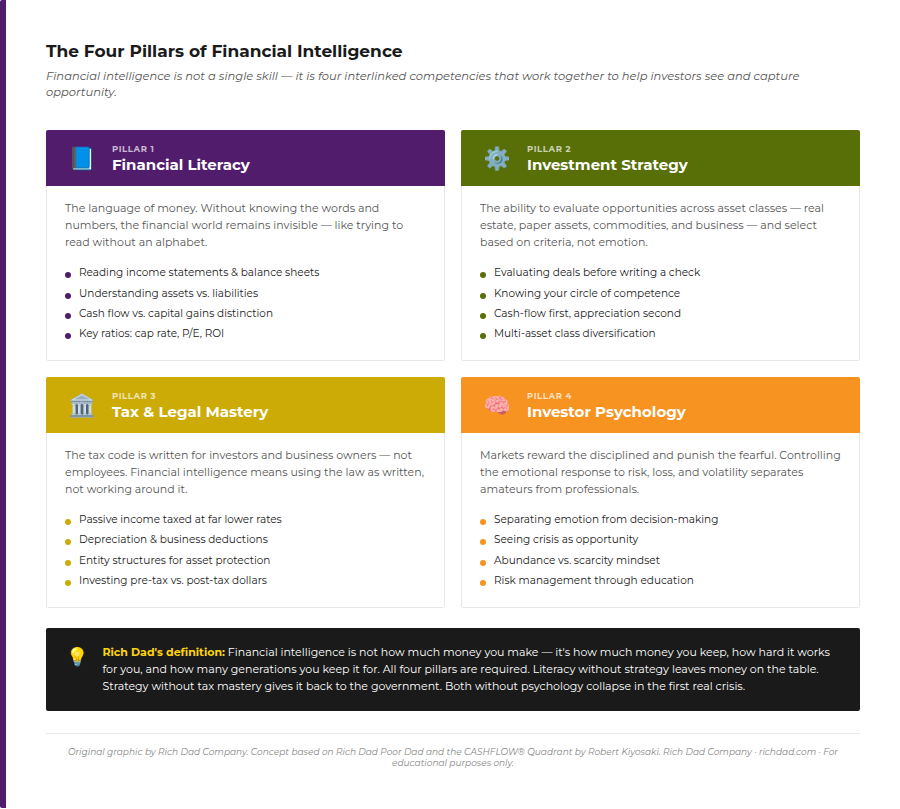

The Four Pillars of Financial Intelligence

Financial intelligence is not a single trait. It is a system of four interlinked competencies that must be developed together. Weakness in any one pillar limits the others.

Pillar 1: Financial Literacy — The Language of Money

Without financial literacy, the rest of the system cannot function. A person who does not understand the difference between a cash-flowing asset and a liability cannot evaluate a real estate deal. Someone who cannot read an income statement cannot assess a business opportunity.

Rich dad’s approach to financial literacy started with the most basic concepts and built from there: how to read a personal financial statement, the difference between income and cash flow, and the meaning of a P/E ratio or capitalization rate. These are not complex concepts — they are simply ones the school system never teaches.

Pillar 2: Investment Strategy — Evaluating Opportunity

Financial literacy tells you what something is. Investment strategy tells you whether to act on it. This pillar encompasses the ability to evaluate deals across real estate, stocks and paper assets, commodities, and business ownership — using defined criteria rather than tips, trends, or emotion.

The Rich Dad framework asks five questions before any investment: Is this inside my circle of knowledge? Does it generate cash flow? What are the tax advantages? What is the real risk — and can I control it? Do I have the right team? An investor who cannot confidently answer all five is not ready to write a check. The unanswered question is an education assignment, not a reason to pass entirely.

Pillar 3: Tax and Legal Mastery — Keeping What You Earn

The United States tax code is not written against investors — it is written for them. Business owners and investors access depreciation, deductions, pass-through structures, and passive loss rules that employees cannot. Personal tax strategies and business tax planning are not loopholes; they are the architecture of the tax code as designed.

According to the IRS Statistics of Income and Tax Foundation data, an employee earning $150,000 in 2025 pays an effective federal rate of approximately 35.7 percent, while an investor earning the same amount through long-term capital gains and passive income pays roughly 15 percent. That 20-point difference — compounded over a career — is the financial intelligence gap expressed in dollars.

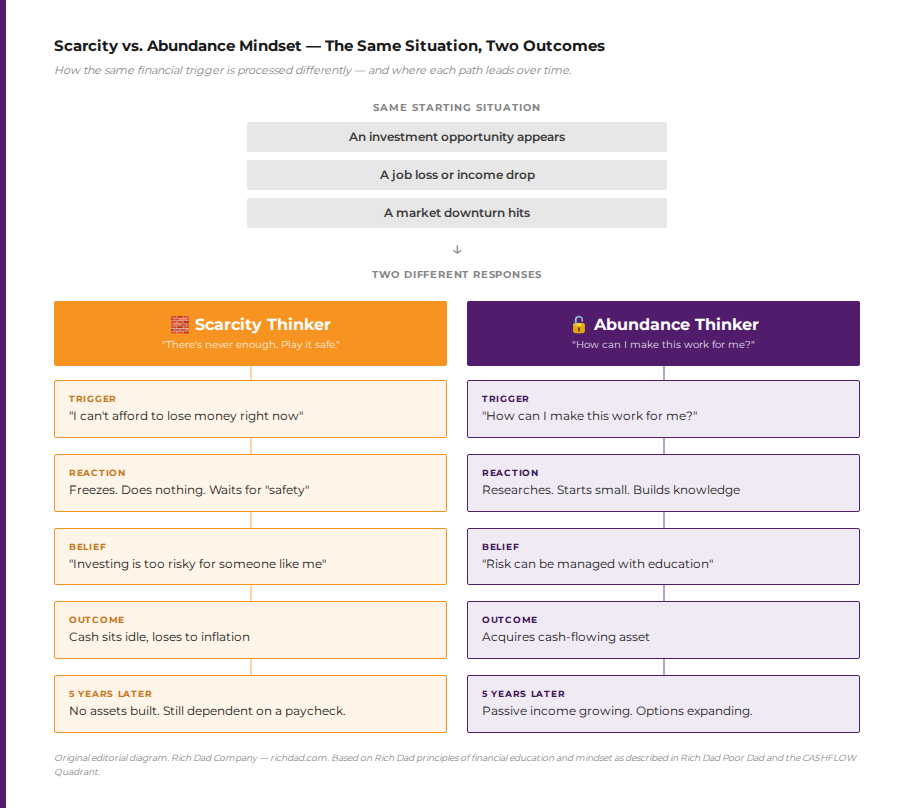

Pillar 4: Investor Psychology — Acting When Others Freeze

Markets are driven by fear and greed. The financially intelligent investor understands this and uses it strategically. When markets fall, the conditioned response is to sell. The educated response is to evaluate whether the fundamentals have changed — and, often, to buy.

This pillar is the one most people overlook. Financial literacy can be taught from a book. Psychology must be practiced through real decisions, real losses, and real lessons. Rich Dad’s approach to building this pillar involves financial simulation — including the CASHFLOW board game — which builds decision-making habits in a safe environment before real capital is at stake.

How Financial Intelligence Reveals Opportunity Others Miss

The 2008 financial crisis and the early months of the COVID-19 pandemic both demonstrated the same pattern: most people contracted in fear while a smaller group expanded into opportunity. The difference was not access to capital — it was access to a framework for understanding what was actually happening.

During the 2008 recession, Robert Kiyosaki identified that government-backed Fannie Mae and Freddie Mac loans remained available even as private credit froze. He used that liquidity to acquire multifamily properties at historically low prices — properties that generated positive cash flow from day one and appreciated significantly over the following years. The opportunity was visible to anyone with the financial education to see it.

During the pandemic’s early weeks, independent sellers on platforms like Etsy generated $133 million in face mask sales during a single month. These were not large corporations with supply chains — they were individuals with the financial intelligence to identify demand and move quickly. Money finds the prepared.

The CASHFLOW Quadrant: Where Financial Intelligence Leads

The CASHFLOW® Quadrant divides the world of income into four categories: Employee (E), Self-Employed (S), Business Owner (B), and Investor (I). The left side — E and S — is driven by security. The right side — B and I — is driven by freedom.

Most people are educated, conditioned, and rewarded to stay on the left side. The school system trains people for employment. The financial media focuses on salary negotiation and retirement accounts. The culture celebrates job promotions. All of this reinforces left-side thinking.

Financial intelligence is what enables the move to the right side. An E or S earner who develops the four pillars — literacy, strategy, tax mastery, and psychology — gradually shifts how income is generated. Assets begin to appear on the balance sheet. Passive income begins to replace earned income. The effective tax rate falls as income sources change.

This is not a fantasy. It is a documented pattern of how the wealthy operate. The question is not whether it is possible. The question is whether a person is willing to invest in the financial education required to execute it.

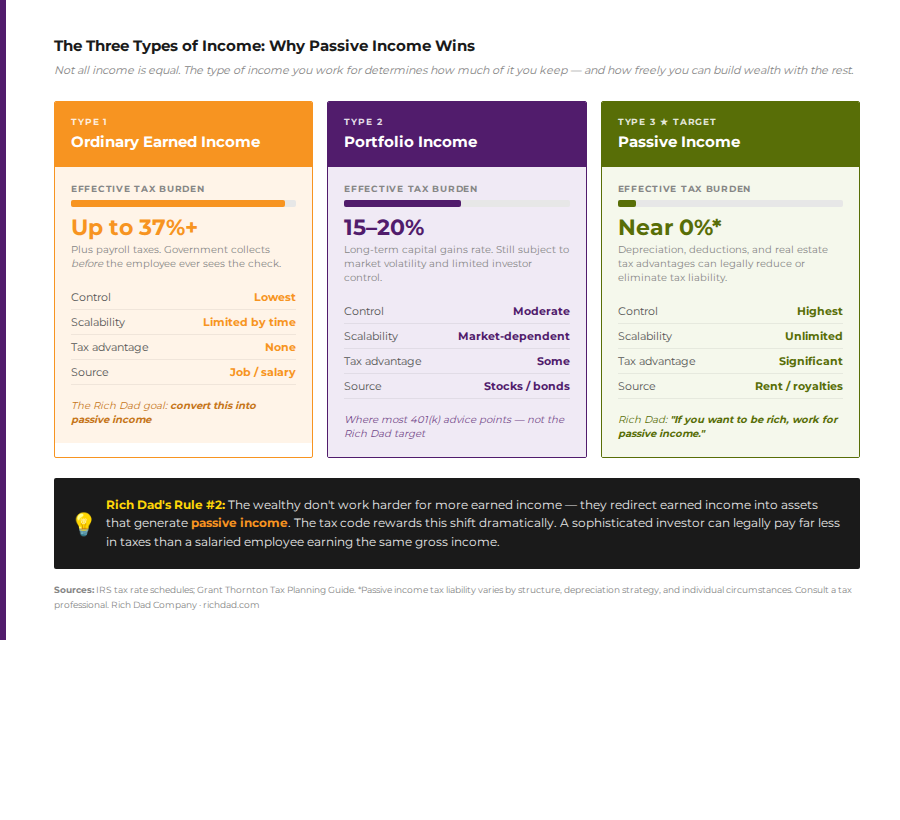

Passive Income and the Three Types of Income

One of the most important distinctions a financially intelligent person learns is the difference between ordinary earned income, portfolio income, and passive income. This is not an accounting classification — it is the basis of the entire Rich Dad philosophy.

Ordinary earned income is taxed at the highest rates and stops the moment the worker stops working. Portfolio income from stocks and funds provides some growth but remains subject to market volatility. Passive income — from rental properties, business distributions, and royalties — carries the most favorable tax treatment and continues regardless of personal activity.

The financially intelligent goal is to redirect earned income into assets that generate passive income — progressively replacing the highest-taxed income type with the lowest. This is not a matter of avoiding taxes; it is using the tax code as designed, for the purposes Congress intended when creating depreciation, deductions, and passive income classifications.

How to Start Building Your Financial Intelligence Today

Financial intelligence is built through a combination of education, simulation, and applied experience. No single book, course, or seminar produces it. It develops over time, through deliberate practice and real-world feedback.

Step 1: Develop Financial Literacy

Begin with vocabulary. Learn the difference between assets and liabilities. Understand how to read a personal financial statement: income, expenses, assets, liabilities. Rich Dad’s free resources at richdad.com are a legitimate starting point, as is the foundational text Rich Dad Poor Dad.

Step 2: Simulate Before You Invest

The CASHFLOW Classic game was designed specifically to teach financial decision-making in a low-stakes environment. Playing repeatedly builds pattern recognition for evaluating deals, managing cash flow, and responding to market events. It is not a game about luck — it is a game about financial education under simulated pressure.

Step 3: Study One Asset Class Deeply

Rather than diversifying too early, Rich Dad recommends developing deep competency in one asset class before expanding. Whether it is single-family rental properties, dividend-paying stocks and options, or small business, mastery of one generates both cash flow and credibility that makes subsequent investments easier to evaluate.

Step 4: Build Your Financial Team

No investor operates alone. The financially intelligent person assembles a team: a CPA who understands investor tax strategy, an attorney specializing in asset protection, and advisors with real-world experience in the chosen asset class. The wrong accountant — one who thinks like an employee — can cost more in lost tax strategy than the fees of the right one.

Step 5: Invest in Ongoing Education

Rich Dad’s courses, memberships, and newsletters are designed to continue financial education past the foundation stage. The Rich Dad Radio Show provides ongoing exposure to expert thinking across real estate, commodities, stocks, and macroeconomics. Financial intelligence compounds — every investment in education increases the return on every subsequent financial decision.

Financial Intelligence in Practice: Crises as Classrooms

History repeatedly demonstrates that financial crises are the proving ground of financial intelligence. The 2008 recession. The COVID-19 economic disruption. The inflationary environment of the early 2020s. In each case, those without financial education experienced primarily loss. Those with it experienced primarily opportunity.

This is not callous — it is structural. When prices fall, distressed assets become available to those with capital and the knowledge to evaluate them. When interest rates rise, cash-flow investing becomes more attractive relative to speculative appreciation plays. When currencies devalue, hard assets like physical gold and silver — which Rich Dad consistently recommends over paper proxies — preserve purchasing power.

The financially intelligent investor is not gambling on outcomes. They are positioning themselves in advance, based on an understanding of how money flows through an economy, which asset classes respond to which conditions, and where value is being created rather than destroyed.

This is the practical definition of financial intelligence: the ability to stay out of fear long enough to see what is actually happening, evaluate it accurately, and act on it deliberately.

Most people are never taught how money works. The school system trains workers, not investors. The financial media markets products, not principles. The result is a population that is 95 percent eyes and five percent mind — looking at piles of opportunity they cannot see.

Changing that starts with a decision: to invest time and effort in a different kind of education. The resources to build financial intelligence are more accessible today than at any point in history. Rich Dad’s library of books, games, courses, and expert podcasts represents decades of practical financial education specifically designed to move people from financial illiteracy toward financial freedom. The only input required from the reader is the willingness to learn.

FAQs

Financial literacy is the foundational ability to understand financial concepts, vocabulary, and numbers — reading a balance sheet, knowing what a P/E ratio means, understanding the difference between an asset and a liability. Financial intelligence is what is built on top of that foundation: the ability to apply that knowledge in real-world decisions, evaluate investment opportunities, manage risk, and position oneself where money is flowing. Literacy is the prerequisite; intelligence is the goal.

Financial intelligence is entirely learned. It is not a trait, a talent, or an inherited characteristic. It develops through deliberate financial education, real-world practice, and feedback from both successes and failures. Rich Dad’s core argument is that the school system does not teach it — which means most people simply have not had the opportunity to develop it, not that they cannot.

The CASHFLOW® Quadrant describes four different ways income can be generated: as an Employee, Self-Employed worker, Business Owner, or Investor. Moving from the left side (E and S) to the right side (B and I) requires a fundamentally different approach to money — one built on financial intelligence. Without the four pillars — literacy, strategy, tax mastery, and investor psychology — the transition is nearly impossible to sustain.

Passive income — from rental properties, business systems, royalties, and dividends — is the only income type that continues when a person stops working. It carries the most favorable tax treatment under the U.S. tax code. And it is the income type that produces financial freedom: the state where monthly passive income permanently exceeds monthly living expenses, making work a choice rather than a requirement.

Rich Dad recommends starting with financial literacy: learning the vocabulary and number systems that make the financial world readable. Reading Rich Dad Poor Dad, playing the CASHFLOW game, and engaging with Rich Dad’s free educational resources at richdad.com are all practical starting points that require minimal investment and provide immediate foundational value.

Economically difficult periods — recessions, market crashes, inflationary environments — consistently create the best opportunities for informed investors. Assets become available at reduced prices. Distressed sellers create buying opportunities. Financially intelligent investors who have studied asset valuation, understand leverage, and have pre-positioned capital can acquire cash-flowing assets that underperforming economic conditions make temporarily accessible. The same event that creates fear in the uninformed creates opportunity for the prepared.