Blog | Personal Finance

Why You Never Have Enough Time to Invest

The poor say, “I’ll have time later.” The rich say, “If I don’t make time now, I won’t have it later.”

December 07, 2021

I’ve frequently written about how savers are losers. And it’s true. In an economy that runs on debt and thrives on inflation (which is red hot while I write this), there is nothing more financially dangerous than thinking your savings will provide a secure financial future.

Well, almost nothing.

The optimism bias

A report issued in 2018 by bankrate.com revealed something even more financially ignorant than relying on savings—thinking you don’t need any savings at all.

The survey revealed that nearly half of respondents didn’t have enough savings to cover three months of living expenses should a financial emergency happen, and 25% had no emergency savings. But perhaps even more alarming was that 18% believed that’s ok and that a financial emergency wouldn’t happen to them.

An article on the survey in USA Today went on to share that this passive attitude to emergency savings most likely comes from the fact that people don’t see others in their life have hard times, and so they don’t think it will happen to them. Psychologists call this optimism bias.

Two types of optimism

I’m a big fan of optimism. In fact, I don’t think you can be successful in life if you don’t have a good dose of it. But there are two kinds of optimism. One type is grounded in reality and the other in fantasy.

Optimism grounded in fantasy says, “Nothing bad is going to happen to me and I’ll always be taken care of so I don’t need to worry about money.” Or perhaps a more dangerous form says, “I know I need to do something about my finances, but I’ll have time to do that later.” Of course, later never comes.

Optimism grounded in reality says, “It is inevitable that I will find myself in hard times financially, but I know that I can outsmart those hard times by investing in my financial education. And if I don’t make time to do that now, I won’t have time to do it later.” This kind of optimism acknowledges reality while also preparing to be the captain of your own financial ship.

Simply put, fantasy optimism trusts in forces outside your control to keep you safe. Realistic optimism trusts in your own ingenuity to keep you safe.

It’s ok to save for a rainy day

Though I often rail against savings, I actually do believe it’s important to have liquid assets on hand should hard times come. Kim and I have six months worth of living expenses available should we reach hard times.

Rather than keep these in cash, we keep them in liquid assets like gold and silver that can be quickly converted to cash if needed.

We do not, however, count on our savings as part of our investing or retirement plans. Rather it is simply there for that rainy day, should it come.

Savings are not enough

When I say savers are losers, I’m talking about those who think savings will be enough to help them have a secure financial future. This is an old way of thinking that doesn’t take into account how money has changed, that it is a currency that loses value if it just sits and isn’t invested.

Because we live in an inflationary economy, cash loses value over time. On the other hand, assets rise and fall in value relative to inflation. If you want to thrive financially, you have to learn how to identify the right investments for your money to flow into and how to find assets that create cash flow. This is what we call investing.

The problem for many, however, is that they think they don’t have time to invest. The real problem is their mindset.

A better way to save money: pay yourself first

There are many differences between the rich and the poor, but one of the more common ones I come across is that of mindset.

For instance, my poor dad always said, “I can’t afford that.” My rich dad said, “How can I afford that?”

My poor dad always said, “Money is the root of all evil.” My rich dad said, “Money is neutral. It’s what you do with it that’s evil or good.”

My poor dad said, “Get a good job so you can have security.” My rich dad said, “Being an employee is the least secure thing you can do.”

One important difference between my poor dad and rich dad was this: My poor dad said, “Save money for a rainy day.” My rich dad said, “Pay yourself first so you’ll never have a rainy day.”

For decades, I’ve followed the advice of my rich dad instead of my poor dad—especially when it comes to paying yourself first. As I wrote in a while back (“Why The Rich Don’t Save Money”):

In order to be rich, you must have the self-discipline to pay yourself first. By this, I simply mean using your income to invest in cash-flowing assets before you pay your bills or buy anything fun. This in turn will create more income that you can use to invest in more, cash-flowing assets. Do that and you’ll have more money than you know what to do with.

Paying yourself first is not easy. In fact, it can be scary, especially when the bills are piling up. But you must develop the self-discipline to do it.

When we were young and trying to build our business, Kim and I did this to great effect. To help us stay accountable, we hired a bookkeeper named Betty. We instructed Betty that each month she was to set aside a portion of our income to be used for investing.

Betty howled with protest each month when we did this because we didn’t have enough money left over to pay our bills. But we told her to keep it up. Instead of worrying about paying all our bills on time, Kim and I spent time renegotiating with creditors, pushing a payment down the road here and there. To us, paying ourselves first was the most important thing, even if Betty and others thought we were crazy.

Kim and I used the money we paid ourselves first to invest in our business and in cash-flowing assets. It’s because of this discipline that we are financially free today.

Paying yourself with time

A while back, I came across a great short article in “The Guardian” that opened my mind to other ways to pay yourself first. Columnist Oliver Burkeman shares an insight he got from reading a blog post by “the cartoonist and creativity coach Jessica Abel". Brakeman’s insight had to do with the principle of paying yourself first as it applies to time:

"If there’s something you’re passionate about—from writing your novel to launching a business to spending more time with your kids—the only way to make it happen is to do a bit of it now, no matter how many urgent tasks are pressing in. “If you don’t save a bit of your time for you, now, out of every week,” Abel writes, “there is no moment in the future when you’ll magically be done with everything and have loads of free time.”

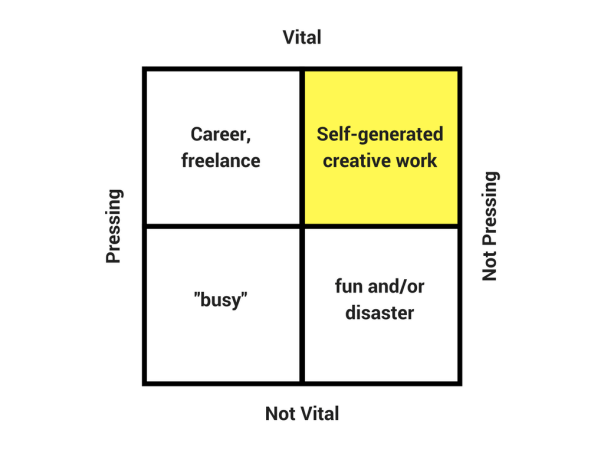

When it comes to business and investing, this concept is as vital as paying yourself first with money. Abel’s shares a matrix from Tim Urban (a modified version of author Stephen Covey’s “Eisenhower Decision Matrix”) on how we use our time in four ways:

In fact, the vast majority of people I talk with who have a hard time getting started with their dreams of starting a business or investing in assets do not have a money problem. Instead, they have a time problem. That is, they spend most of their time on busy tasks, their careers, and doing fun activities. Most people spend little-to-no time on “self-generated creative work.”

Why is this?

It’s not that people don’t have good intentions to do what they are dreaming of. It’s that they always think they’ll have more time than they really do. With money, if you pay everyone else first rather than yourself, you’ll have nothing left to actually invest. The same is true with time.

The rich find time by making time

The Rolling Stones famously sang, “Time is on my side.”

Yes, it is.

One difference in mindset between the poor and the rich is that the rich always seem to find time. It’s been my experience that they do not have time because they have money, but rather they have money because when they were poor they found the time to invest in themselves and their dreams. The rich recognize that they own their time. The poor let others take their time.

The fundamental shift you need to make today if you want to accomplish your dreams of investing or starting a business is to understand that you, and no one else, has a claim on your time. Start paying yourself first with it.

Block time and distraction to achieve your dreams

One simple and practical way to do this is simply to block the time off on your calendar. I know one friend who spends time on Sunday nights to block his calendar off for projects he wants to work on during the coming week. He treats those times on his calendar as sacred, often finding a place to execute on the work he planned in solitude so as not to get distracted or interrupted.

We live in a world that is always trying to steal our attention. In fact, attention has become one of the most precious commodities in the information economy. So, my friend also often turns off his phone, web browser, and email, to accomplish his work and tasks. And you’ll rarely see him on Facebook.

By taking these simple actions, most people can create the time and attention they need to work towards accomplishing investing and business goals, even while working full-time. All it takes is truly believing your time is your own and no one else—and doing something about it.

Original publish date:

March 13, 2018