Without financial education, you’re just gambling

Every year, Americans spend billions on lottery tickets, casino visits, and sports betting — all in the hope that luck will solve a financial problem that education could actually fix. According to the American Gaming Association, U.S. commercial casinos generated a record $66.5 billion in revenue in 2023. Meanwhile, a TIAA Institute survey found that only 57% of Americans demonstrate basic financial literacy. The connection between those two statistics is not a coincidence.

Managing money effectively is not about willpower, income level, or getting lucky on a trade. It is about financial education — understanding how money moves, what makes an asset versus a liability, and how to build income streams that work independently of any one job, market condition, or fortunate break.

As Robert Kiyosaki laid out in Rich Dad Poor Dad, the game of money has rules, and those rules can be learned. This guide brings those principles together in a practical framework for managing money with intention and intelligence.

Why most people struggle to manage their money

The financial system was not designed to build individual wealth — it was designed to build institutional wealth. The average person is conditioned from childhood to earn a paycheck, deposit it in a bank, contribute to a 401(k), and hope for the best at retirement. We call this the rat race — a cycle of working for money rather than having money work for you.

The truth about savings accounts

Keeping money in a savings account feels responsible. But with interest rates that consistently lag behind inflation, a savings account is less a wealth-building tool and more a slow drain on purchasing power. When a government prints money to stimulate economic activity, each dollar already in savings quietly buys less. Savers are losers in an inflationary environment — not because saving is wrong, but because saving alone, without investing, guarantees a loss of value over time.

The hidden costs of mutual funds

Mutual funds are marketed as diversified, professionally managed investments. In practice, they are fee-heavy vehicles that, as Vanguard founder John Bogle famously observed, transfer the majority of long-term returns from investors to the financial industry. Expense ratios, load fees, and fund turnover costs quietly erode compounding gains over decades. The investor bears all the risk but collects only a fraction of the reward.

The 401(k) problem

The 401(k) is perhaps the most widely trusted and least understood financial product in America. Contributions are automatic, the tax deferral feels like a benefit, and the employer match appears to be free money. But the 401(k) carries a hidden tax time bomb — deferred income taxed at whatever rate the government sets at withdrawal — along with limited investment options, fund manager fees, and zero control. For a deeper look at the structural problems with this retirement vehicle, see Rich Dad’s personal finance hub.

Money management vs. gambling: understanding the difference

This following is not a metaphor. Relying on financial instruments that cannot be understood, adjusted, or actively managed is structurally similar to placing a bet. The outcome may be positive — but it is not predictable, repeatable, or within the investor’s control. That absence of control is exactly what makes an approach speculative rather than strategic.

Cash flow investing — whether through real estate, paper assets, a business, cryptocurrency, or commodities — involves risk, too. The difference is that with financial education, risk can be studied, measured, and managed. An investor who understands a rental property’s cash-on-cash return, vacancy rate, and local market dynamics is not gambling. An investor who puts retirement savings into a target-date fund and checks back in 30 years is closer to it than most financial advisors would admit.

How to manage your money: The Rich Dad Framework

Rich Dad’s approach to money management is not a budget app or a savings challenge. It is a system built on financial intelligence — the ability to read your own financial position clearly and make decisions that increase assets and cash flow over time. The full framework is explored in depth across Rich Dad’s personal finance education hub. Here is how it works in practice.

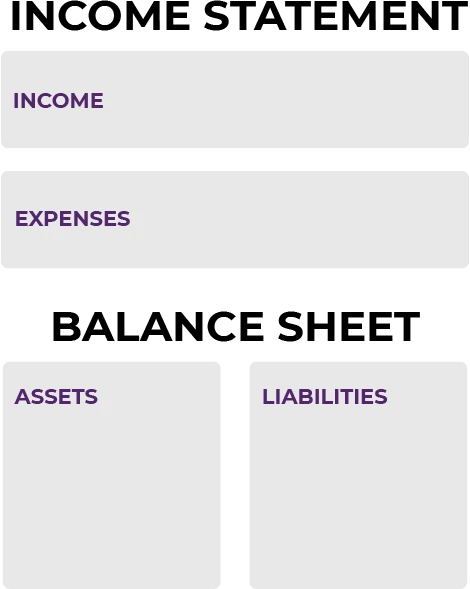

Step 1: Master your personal financial statement

Before any investment decision is made, any budget is built, or any debt is addressed, a person needs to know exactly where they stand financially. The personal financial statement captures four interconnected pieces of information: income, expenses, assets, and liabilities.

Most people have a rough sense of their income and expenses. Far fewer can accurately identify their assets and liabilities — largely because the conventional definition is wrong. Rich Dad’s definition is precise: an asset puts money in your pocket. A liability takes money out. By this definition, a primary residence is a liability, not an asset. A car is a liability. Only investments that generate positive cash flow qualify as true assets.

Step 2: Know what you actually own

Once the personal financial statement framework is clear, the next step is an honest audit. Most people discover that a significant portion of what they assumed were assets — their home, their car, their retirement account — are actually liabilities or illiquid instruments with minimal control. True assets in the Rich Dad framework include income-producing real estate, dividend-generating stocks, businesses that generate cash flow without requiring constant owner presence, and paper assets like options that produce regular income.

This reframe changes everything about how money decisions are made. Rather than asking “how do I save more?”, the question becomes: “how do I acquire more assets that pay me each month?”

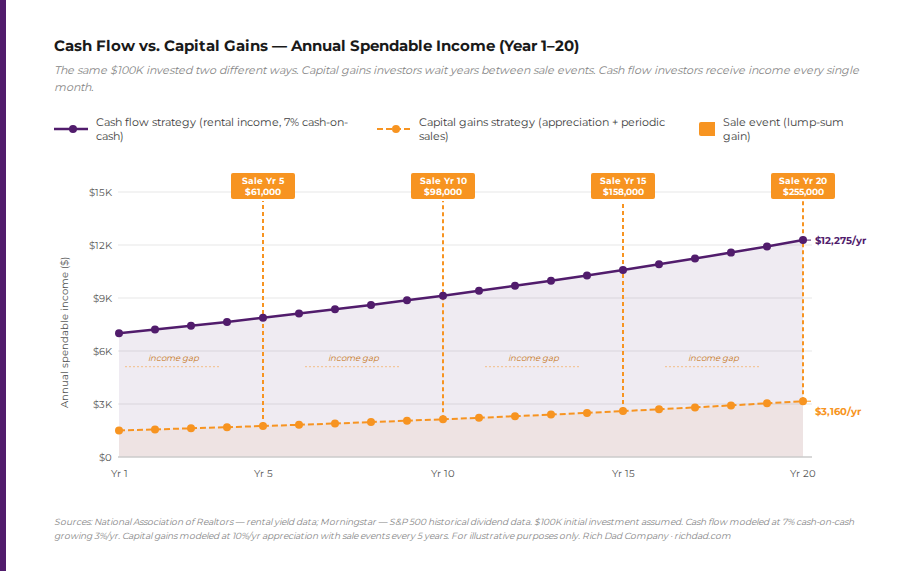

Step 3: Choose cash flow over capital gains

There are two ways to make money from investments: capital gains and cash flow. Capital gains come from buying low and selling high — a strategy that requires perfect timing, ongoing market participation, and willingness to exit positions. It works in bull markets. It is punished in bear markets. And it requires constant repetition to sustain income.

Cash flow investing generates recurring income from a held asset — monthly rent from a property, quarterly dividends from a stock, or premium income from a covered call options strategy. Cash flow does not require selling. It does not depend on market timing. It compounds when reinvested.Rich Dad’s StockCast with Andy Tanner covers these paper asset cash flow strategies in depth.

Step 4: Use debt strategically

Most financial advice treats all debt as a problem to eliminate. Rich Dad makes a more important distinction. Bad debt is borrowed money used to purchase liabilities — credit card balances, car loans, personal loans for consumer spending. Good debt is borrowed money used to acquire assets that generate cash flow exceeding the cost of the debt. A mortgage on a rental property generating $400 in monthly cash flow after all expenses is not a burden — it is a wealth-building tool. This distinction is explored fully in Rich Dad’s debt management guide.

Step 5: Invest in financial education before anything else

No investment strategy works without the foundation of financial education. This does not mean a college degree or a financial planning certification. It means learning to read a financial statement, understanding how different asset classes generate returns, and studying how taxes work for investors versus employees. Rich Dad’s most accessible entry point is the free CASHFLOW Classic game — designed to simulate the financial decisions that separate people who escape the rat race from those who remain trapped in it.

Practical money management tips grounded in financial intelligence

The Rich Dad framework is a philosophy, but it translates into concrete daily habits and decision patterns. Here are the practices that consistently separate people who build wealth from those who wonder where their money went.

Track every dollar against the financial statement

Rich Dad’s budgeting philosophy focuses less on cutting expenses and more on directing every dollar either toward liability reduction or asset acquisition. A person who earns $60,000 a year and systematically converts 20% of income into cash-flowing assets will outpace a person earning $100,000 who directs spending toward consumer liabilities, every time.

Reduce taxes through financial intelligence

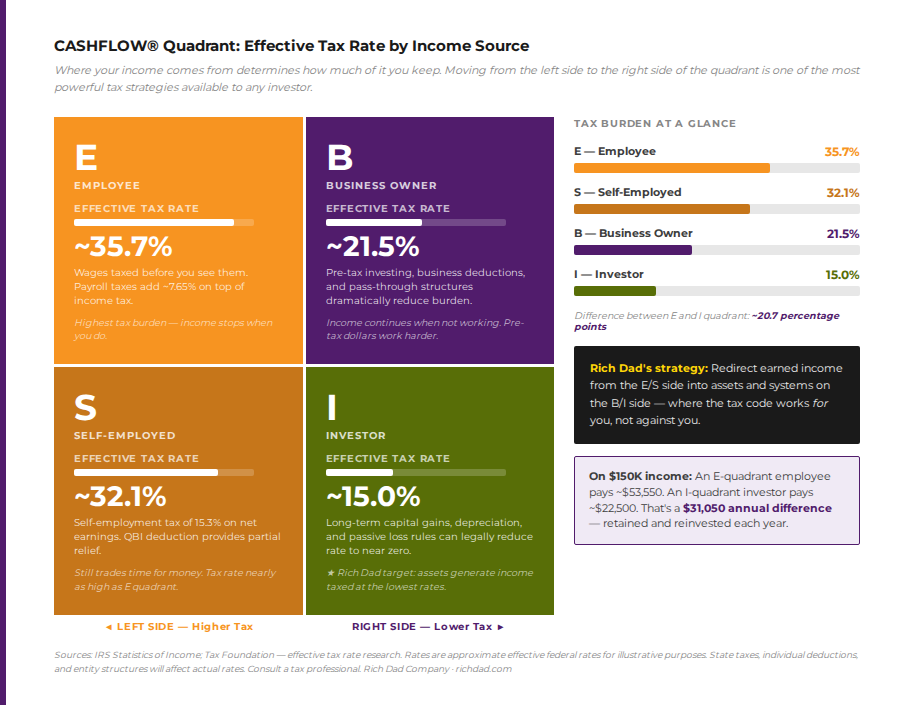

Employees pay the highest effective tax rates of any income earner. Business owners and investors have access to legal tax strategies — depreciation, entity structuring, tax-advantaged accounts, and timing strategies — that dramatically reduce what the government takes. Understanding how taxes work at each quadrant of the CASHFLOW Quadrant is a core component of effective money management. Rich Dad covers this across both personal tax strategies and business tax planning. For expert-level tax strategy, The WealthAbility Show is an invaluable ongoing resource.

Build multiple income streams

One income stream is a single point of failure. Rich Dad consistently emphasizes building across asset classes —real estate for cash flow and appreciation, paper assets for liquidity and dividend income, business ownership for scalable earnings, and commodities as an inflation hedge. This is not just risk management — it is building a financial infrastructure that does not depend on any single employer, market, or economic cycle.

Only invest in what you understand

When an investor does not understand what they own, they cannot evaluate whether the investment is performing, identify warning signs, or make adjustments. Handing money to a fund manager and checking back in a decade is not investing — it is hoping. Financial education creates the capacity to evaluate, select, and actively monitor investments across every asset class.

The bottom line: Managing money is a skill, not a personality trait

People who manage money well are not more disciplined, more naturally talented, or luckier than average. They have learned the rules of the financial game that most people were never taught. They can read a financial statement. They know the difference between an asset and a liability. They understand how cash flow works across different asset classes. And they use that knowledge to make decisions that consistently move money toward financial independence rather than away from it.

The alternative — handing money over to institutions that benefit from limited financial literacy, contributing to retirement accounts with no understanding of the underlying mechanics, and hoping for the best — is the financial equivalent of gambling. The odds are not in favor of the uninformed.Financial education is the house advantage that individuals can acquire for themselves. Start with the free CASHFLOW Classic game, explore the personal finance hub, and take the Investment IQ assessment to identify where the gaps in your financial knowledge currently are. Managing money well is not about luck. It never was.

FAQs

The first step is creating an accurate personal financial statement that tracks income, expenses, assets, and liabilities. Without a clear picture of your current financial position, it is impossible to make sound money decisions. Rich Dad’s framework begins here because financial clarity is the foundation of all wealth-building activity.

The core difference is control. Gambling surrenders money to chance. Investing with proper financial education involves evaluating risk, understanding an asset’s mechanics, and making decisions that can be monitored and adjusted. An investor who understands their asset’s fundamentals is exercising control — not relying on luck.

Capital gains are profits realized when an asset is sold at a higher price than it was purchased. Cash flow is recurring income generated by a held asset — rent, dividends, or options premium income. Rich Dad prioritizes cash flow because it generates ongoing income without requiring a sale and is not dependent on market timing.

A 401(k) offers tax-deferred growth and sometimes an employer match, but Rich Dad identifies key limitations: investors surrender control to fund managers, fees compound silently, investment options are restricted, and the deferred tax creates a future liability at an unknown rate. Relying on a 401(k) exclusively carries more risk than most participants realize.

Bad debt buys liabilities — things that take money out of your pocket. Good debt acquires cash-flowing assets where the return exceeds the cost of borrowing. A mortgage on a cash-flow-positive rental property is good debt. A credit card balance on consumer spending is bad debt. Rich Dad treats debt as a tool — powerful when used strategically, destructive when used carelessly.

Start by learning to read a personal financial statement. Then play the free CASHFLOW game at richdad.com/cashflow/ to build financial intuition in a no-risk environment. From there, explore Rich Dad books, podcasts, and the investing education hub to progressively deepen your knowledge and make better money decisions over time.

In an inflationary environment, money sitting in a low-yield savings account loses purchasing power every year because interest rates rarely keep pace with inflation. Rich Dad’s position is that money should be put to work in assets that appreciate or generate cash flow — not left dormant in accounts that benefit the bank far more than the account holder.