Make your money work for you

Here’s something that might surprise you: If you’re stressed about money, it’s not because you’re doing something wrong. It’s because you’re in the wrong place.

Rich dad used to tell Robert something that seemed crazy at the time: “The poor and middle class work for money. The rich make their money work for them.”

But here’s what Robert didn’t fully understand back then—this isn’t just about making money. It’s about why some people lose sleep over their finances while others sleep peacefully, even during economic chaos.

Error: Campaign not found.

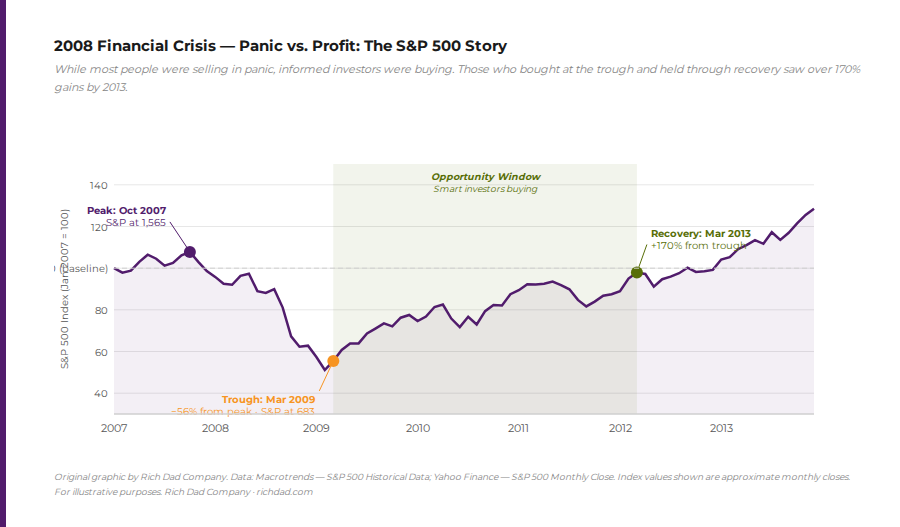

Think about it. During the 2008 financial crisis, millions of people were stressed about money— losing their homes, their jobs, their retirement savings. But some people weren’t just surviving; they were thriving. They were buying real estate at rock-bottom prices, investing in stocks when everyone else was selling, and building businesses while their competitors were closing down.

What was the difference? Position.

The stress you feel has nothing to do with how much you make

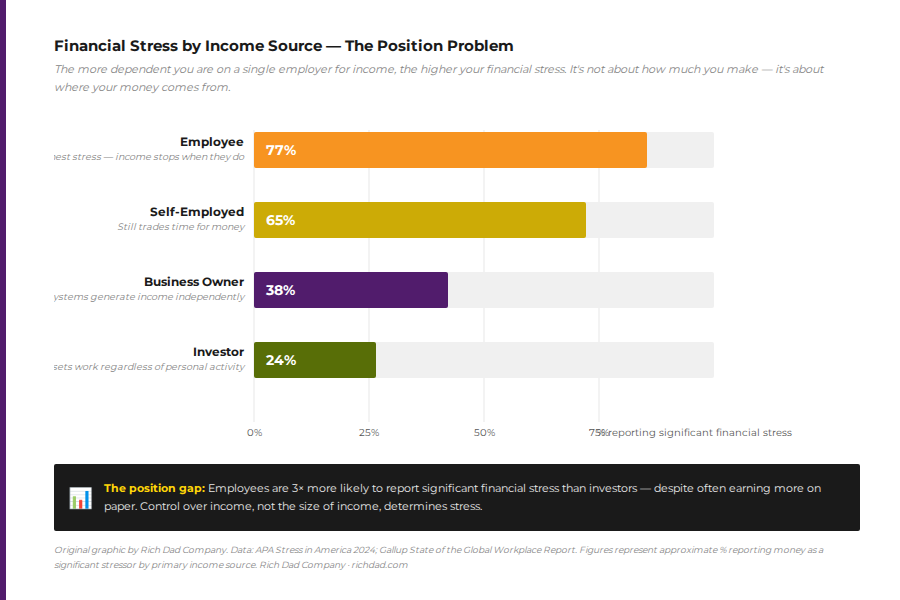

The Rich Dad Company has been teaching this for decades, and it still shocks people: Your stress about money has very little to do with how much money you make. We’ve met six-figure earners who can’t sleep at night and cash flow investors who are completely relaxed, even though they might make less on paper.

Why? Because stress about money comes from three fundamental problems that have nothing to do with your paycheck size.

Problem #1: You’ve been given terrible financial advice

Let’s be honest about something. The financial advice most people follow is setting them up for a lifetime of money stress. “Go to school, get a good job, save money, buy a house, invest in mutual funds for the long term.” Sound familiar?

This is the advice that’s supposed to lead to financial security. Yet according to studies, over half of American employees report being stressed about their finances. If this advice worked, wouldn’t the stress be going down instead of up?

Here’s what Rich Dad knew that most “financial experts” miss: A high-paying job isn’t security— it’s a beautiful trap. The higher your salary, the more dependent you become on that salary. And the more dependent you are, the more stressed you’ll be about losing it.

Take the recent economic turbulence. Millions of people with “secure” jobs discovered that their security was an illusion. Meanwhile, people who had built passive income streams through businesses and investments were not only fine—many were finding new opportunities.

Problem #2: You have zero control over your financial future

This is where it gets uncomfortable. If you’re an employee, you have almost no control over your financial destiny. You can’t control when you get laid off. You can’t control when your company gets bought or goes under. You can’t control when the economy shifts and your industry disappears.

You’re basically a passenger on someone else’s financial airplane, and that’s terrifying.

Even if you have stock options, you probably don’t have real control. Most companies issue different classes of stock, and guess which class employees get? The one without voting power.

Business owners and investors keep the control for themselves because they understand what employees don’t: Control equals security.

But here’s what’s interesting. When Robert talks to successful business owners and investors, they’re rarely stressed about money. Why? Because they have control. If one income stream dries up, they can create another. If one investment goes bad, they have others. If the economy shifts, they shift with it.

Control doesn’t eliminate challenges—it eliminates the helpless feeling that creates money stress.

Problem #3: You’re playing a rigged game (and nobody told you)

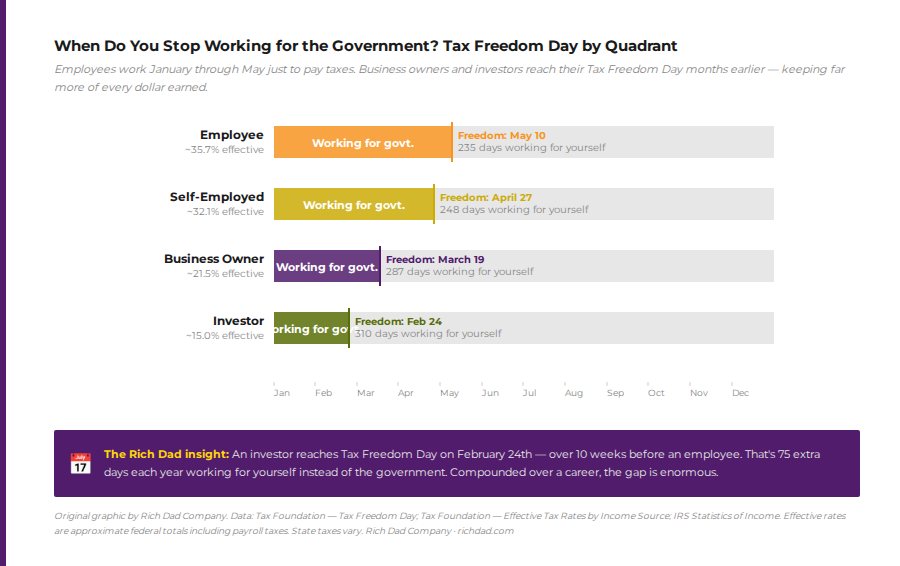

Want to know why you feel like you’re working harder but getting nowhere? Because the tax system is designed to extract the maximum amount from employees while giving business owners and investors every possible break.

This isn’t a conspiracy theory—it’s tax law. Employees pay the highest tax rates on earned income. Business owners and investors pay the lowest rates on passive income. And there’s almost nothing you can do about it as an employee.

Rich Dad called this “working for the government.” Because when you really break down an employee’s paycheck, they’re working January through May just to pay taxes. Meanwhile, sophisticated business owners and investors are using legal strategies like depreciation and business expenses to dramatically reduce their tax burden.

This isn’t fair, but it’s reality. And fighting reality is exhausting.

The CASHFLOW Quadrant: Why your position determines your stress level

Rich Dad’s CASHFLOW Quadrant explains everything you need to know about money stress. On the left side, you have Employees (E) and Self-Employed (S) people. On the right side, you have Business Owners (B) and Investors (I).

Left side = high stress. Right side = low stress.

Error: Campaign not found.

It’s that simple.

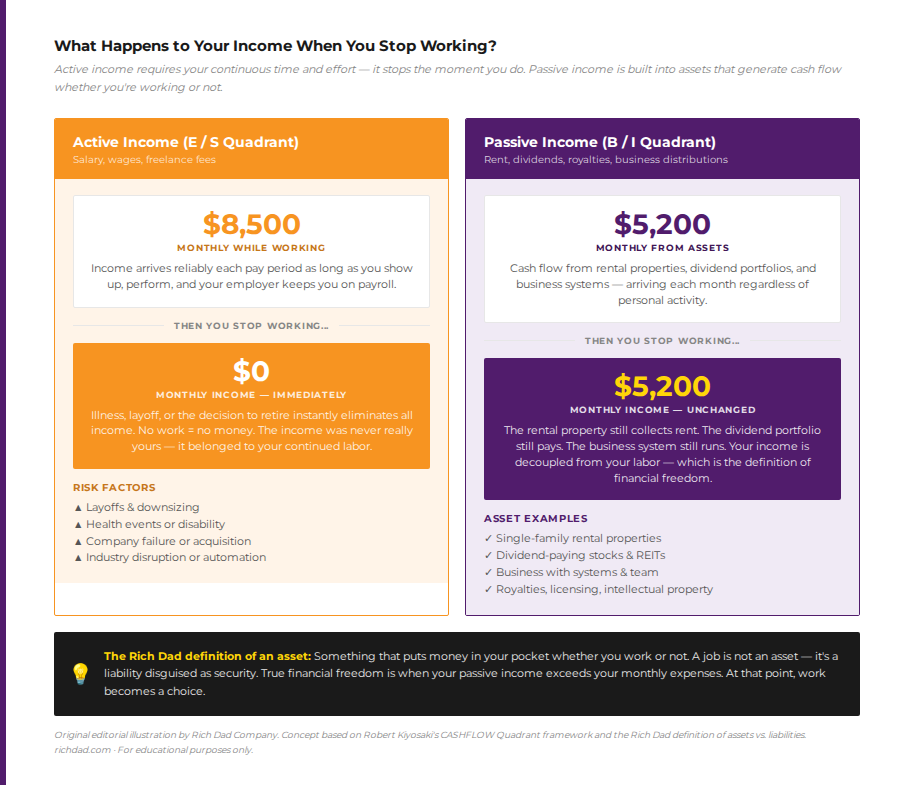

People on the left side trade time for money. If they stop working, the money stops. They have no control, pay the highest taxes, and live in constant fear of what happens if they can’t work.

People on the right side make their money work for them. They’ve built assets that generate cash flow whether they’re working or not. They have control, pay lower taxes, and sleep well because their financial security doesn’t depend on their physical ability to work.

This is why a real estate investor with a few rental properties often has less money stress than a highly paid surgeon. The surgeon’s income dies if the surgeon dies. The rental properties keep producing income regardless.

How rich people handle financial turbulence

Here’s something most people don’t understand about wealthy investors and business owners: They face the same economic turbulence as everyone else. Stock markets crash for them too. Recessions affect their businesses. The difference is how they respond.

Poor and middle-class people try to avoid turbulence. They seek “security” and “safety.” Rich people expect turbulence and prepare for it. When it comes, they don’t panic—they profit.

Robert learned this lesson from Rich Dad early on. “Turbulence isn’t your enemy,” Rich Dad would say. “It’s your opportunity. When everyone else is panicking, that’s when the real deals appear.”

During the 2008 crisis, while most people were stressed about money and trying to hold onto what they had, smart investors were buying distressed properties, starting businesses with laid off talent, and positioning themselves for the recovery.

The key is having a system for handling turbulence instead of avoiding it.

Your turbulence response system

When financial turbulence hits—and it will—here’s how to respond like a rich person instead of panicking like most people:

- Step 1: Breathe and assess

What exactly happened? Get specific. “The market crashed” isn’t helpful. “My tech stocks lost 20% value” is actionable information. - Step 2: Ask the right questions:

- What can I control right now?

- Who in my network has experience with this situation?

- What information do I need to make a smart decision?

- What opportunities might this turbulence create?

- Step 3: Take action

Rich people don’t freeze when turbulence hits. They move quickly with the information they have. Perfect information doesn’t exist, but successful people act on good enough information. - Step 4: Learn and adjust

Every piece of turbulence teaches you something. Extract the lesson and apply it to your financial education.

The path from stressed to successful

Moving from the left side of the quadrant to the right side isn’t just about making more money— it’s about changing your entire relationship with money. Instead of being stressed about money, you become excited about opportunities.

Error: Campaign not found.

But here’s the hard truth: This transition requires financial education that most people never get. Schools don’t teach this. Traditional financial advisors often don’t understand this. You have to seek it out yourself.

Start by changing how you think about income. Instead of just trying to earn more money from a job, start building assets that generate cash flow. Read Rich Dad Poor Dad if you haven’t already. Play CASHFLOW to practice investor thinking in a safe environment.

Most importantly, start surrounding yourself with people who think like business owners and investors instead of employees. Your financial IQ will rise to match the people you spend time with.

The bottom line on money stress

Being stressed about money isn’t a character flaw—it’s a position flaw. You’re in the wrong quadrant, playing by the wrong rules, with the wrong education.

The good news? You can change quadrants. It takes time, education, and commitment, but it’s absolutely possible. And once you do, you’ll discover something amazing: Money stops being a source of stress and starts being a source of freedom.

Remember what Rich Dad taught Robert: “The poor and middle class work for money. The rich make their money work for them.”

When money works for you through passive income and cash flowing assets, stress transforms into excitement, problems become opportunities, and financial turbulence becomes your competitive advantage.

The choice is yours. You can stay stressed about money on the left side of the quadrant, or you can join the business owners and investors on the right side who sleep well at night because they’ve built real financial security.

Which side will you choose?

FAQs

Money stress comes from your financial position, rather than your actual income. Relying on a job for a paycheck creates anxiety, while owning cash-flowing assets provides stability.

The quadrant shows that Employees (E) and Self-Employed (S) individuals tend to experience more stress because they trade time for money, while Business Owners (B) and Investors (I) build systems and assets that generate income regardless of their time.

The first step to reducing money stress is to build financial education and acquire assets that produce cash flow, rather than relying solely on earned income. Examples include small businesses, investments, or real estate. Remember, small steps toward ownership create greater control over time.

Shift your focus from earning money to making money work for you, a principle emphasized in This is the only way you can replace uncertainty with control; by turning money from a source of fear into a source of freedom.