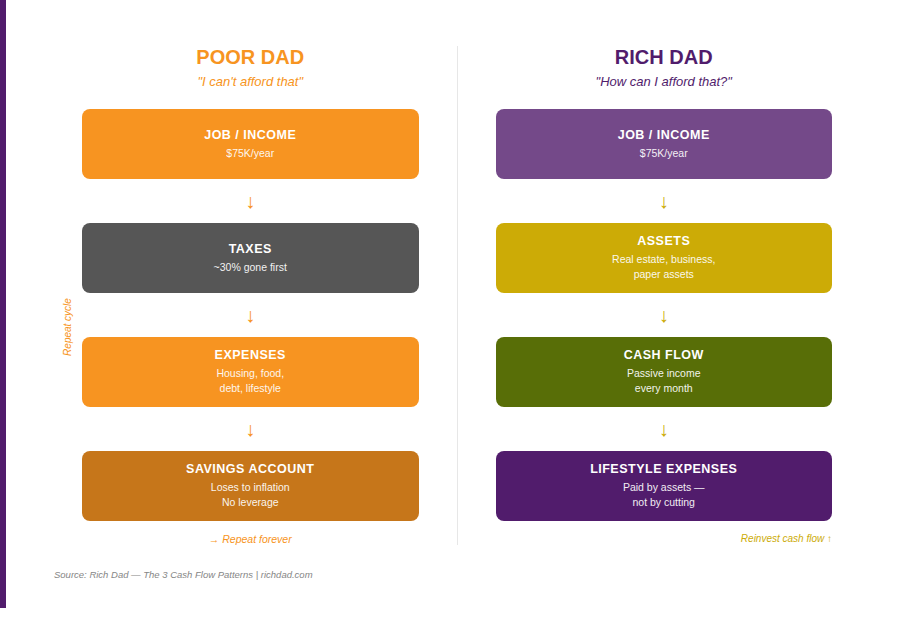

What is the difference between an asset and a liability?

Most people have a vague understanding of the words “asset” and “liability.” Accountants define an asset as anything with economic value that an entity owns. Under that accounting definition, yes — a house is listed in the asset column. But Rich Dad offers a more useful definition, one that actually predicts whether a person is building wealth or consuming it.

The Rich Dad definition is simple: an asset puts money in your pocket. A liability takes money out of your pocket. That is it. That is the entire test. Not what accountants say. Not what the bank calls it on a balance sheet. What happens to your cash every month.

By this definition, assets include rental properties that generate monthly rent, dividend-paying stocks, businesses that produce income, and commodities that produce royalties. Liabilities include debt, expenses, and anything that requires a cash outflow without producing a cash inflow — including, in most cases, the home you live in.

Understanding the difference between assets and liabilities is the foundation of everything Rich Dad teaches. Without it, people cannot make sense of why the rich get richer while middle-class families with good incomes and nice homes seem to make no financial progress.

Your house isn’t an asset

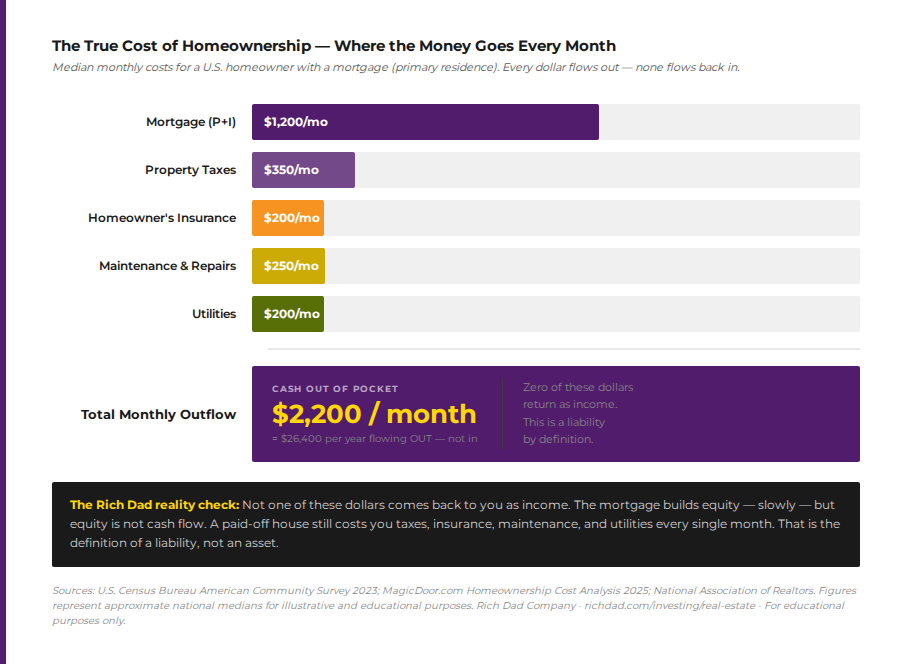

Apply the cash flow test to a typical primary residence and the answer emerges immediately. Every month, money leaves the homeowner’s pocket in the form of a mortgage payment, property taxes, homeowner’s insurance, maintenance costs, and utilities. According to MagicDoor’s 2025 homeownership cost analysis, the average annual cost of homeownership — including maintenance, taxes, and insurance — is approximately $18,000, or around $1,500 per month. For homeowners who purchased recently and carry higher mortgages, the U.S. Census Bureau’s American Community Survey puts median monthly housing costs for mortgaged homeowners at over $2,000.

Not one of those dollars returns to the homeowner as income. The home produces nothing. No rent. No dividends. No royalties. Just an ongoing outflow that does not stop until the house is sold — and even a paid-off home continues to generate property taxes, insurance, maintenance, and utilities for as long as the owner lives in it.

Before it’s your’s, it’s the bank’s asset

There is another layer to consider for the majority of homeowners who carry a mortgage. Before the house is paid off, it is not actually the homeowner’s asset — it is the bank’s asset. The bank lent the money. The bank collects interest on top of principal repayment every month. If a homeowner looks at an amortization table for their mortgage, they will find that in the early years, the majority of each payment goes to interest — income that flows directly to the lender.

If the homeowner defaults, the bank keeps the house and all the payments already made. The bank’s investment is secured. It earns a reliable monthly return. That is the very definition of an asset — for the bank. The homeowner, meanwhile, is paying for the privilege of building the bank’s wealth while being told they are building their own.

Financial advisors often counter this by pointing to three benefits: paying down principal (which builds equity), mortgage interest deductions (which reduce taxes), and appreciation (which can increase the sale price). Rich Dad addresses each directly. Paying down principal is a form of forced savings — and as Robert Kiyosaki has said, savers are losers in an era of inflation, low interest, and missed investment opportunities. The mortgage interest deduction rarely offsets total housing costs. And appreciation, as the next section explains, is not a financial strategy — it is a gamble.Your house isn’t an asset

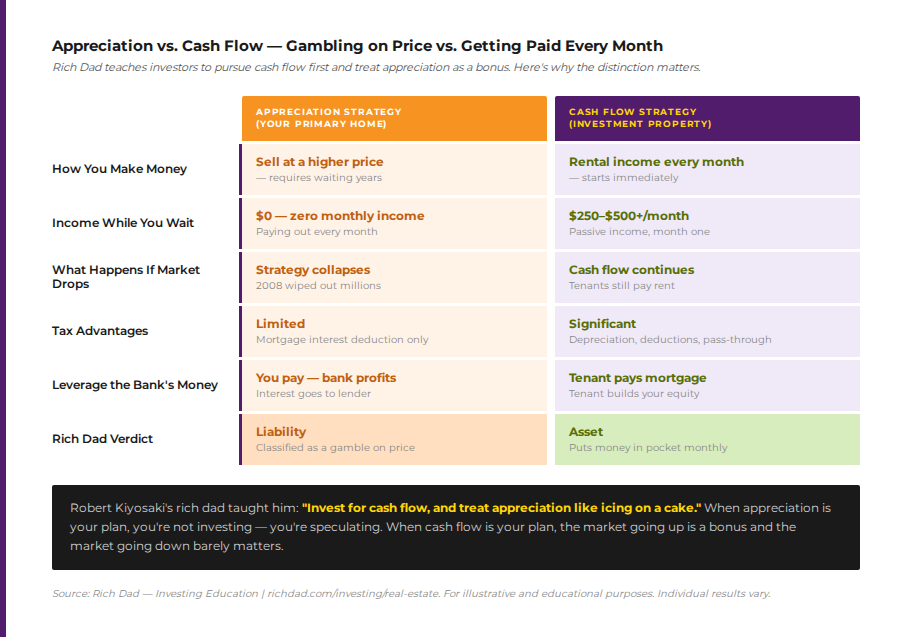

“But my home has gone up in value” — The Appreciation Trap

The most common objection to the Rich Dad position is appreciation: “My house was worth $250,000 when I bought it, and now it’s worth $500,000. How is that not an asset?” It is a fair question that deserves a direct answer.

First, unrealized appreciation is not income. The house is worth more on paper, but no cash has entered the owner’s pocket. The home still costs money every month. To access that appreciation, the owner must either sell the house — giving up the place they live — or borrow against it through a home equity loan, creating new debt.

Second, appreciation is not guaranteed. The homeowners who bought near the 2006 peak discovered this catastrophically. According to the Federal Reserve, U.S. home prices dropped an average of 33 percent nationally during the 2008 financial crisis, with some markets declining by more than 50 percent. Those who had been treating their homes as appreciating assets — borrowing against equity to fund their lifestyles — were devastated. No amount of financial planning recovered the years, the wealth, and in many cases the credit that were lost.

Third, the Rich Dad philosophy does not say appreciation never happens. It says do not build a financial strategy around it. Rich dad taught Kiyosaki to invest for cash flow and treat appreciation like icing on a cake. That icing may arrive — but a person cannot build financial freedom on icing alone.Before it’s your’s, it’s the bank’s asset

How to make a house an actual asset

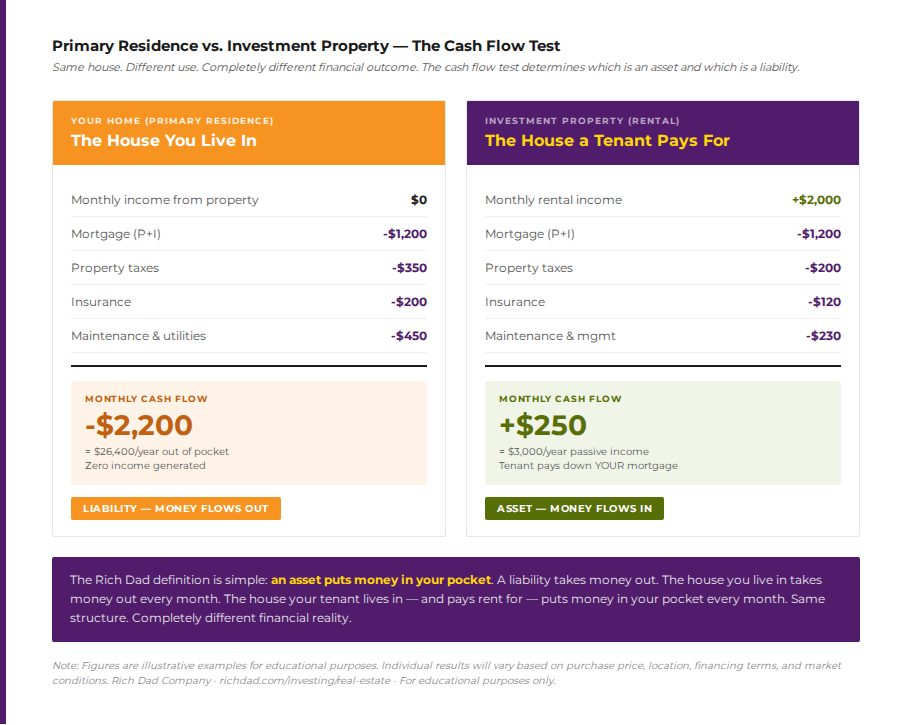

This position is not anti-real estate. It is pro-cash flow real estate. And the distinction is critical. A house can absolutely become an asset — the moment it starts generating income that exceeds its expenses.

This happens in one primary way: investment property. When a property is rented out, a tenant pays rent. That rent covers the mortgage, taxes, insurance, and maintenance — and in a properly evaluated deal, leaves money left over. That leftover is positive cash flow, and positive cash flow is the definition of an asset.

The tenant is, in effect, paying down the owner’s mortgage while the owner collects cash. The owner also benefits from depreciation deductions that can significantly reduce taxable income from the property. Over time, rent tends to rise with inflation while the mortgage payment stays fixed — widening the cash flow margin year after year. This is the model behind Rich Dad’s approach to real estate investing.

There are also strategies that allow a primary residence to generate partial income — renting out a spare room or accessory dwelling unit, for example. In those cases, the home moves along a spectrum toward an asset to the extent that income offsets its costs. But the home the owner lives in and pays for entirely remains, by definition, in the liability column.

Cash flow vs. appreciation: Choosing the right strategy

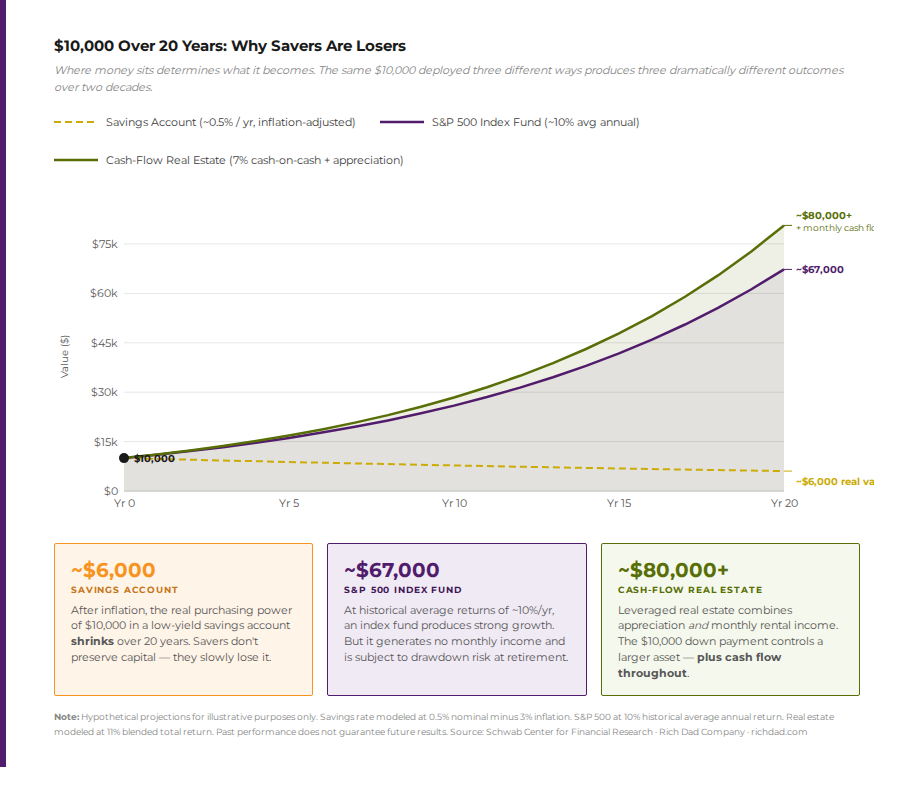

Understanding whether a house is an asset leads directly to the next question: what is the right real estate strategy? Rich Dad makes the answer clear — invest for cash flow, not for appreciation.

A cash flow strategy begins producing income from day one. It is resilient to market downturns because tenants continue paying rent even when property values decline. It offers substantial tax advantages through depreciation and operating expense deductions that appreciation-focused investing does not. And it builds toward financial freedom — the point at which passive income from assets permanently exceeds monthly living expenses — in a concrete, measurable way.

An appreciation strategy requires waiting. It produces no income during the holding period. It is entirely dependent on market timing and external forces outside the investor’s control. And as multiple historical cycles have demonstrated, it can reverse catastrophically at exactly the wrong moment.How to make a house an actual asset

Where your home belongs on the financial statement

Rich Dad uses the personal financial statement as a teaching tool to make abstract ideas concrete. Every dollar either flows into the income column from an asset, or flows out of the expense column toward a liability. The question is always: which direction does this item send cash?

A personal residence sits on most people’s balance sheets in the asset column — that is standard accounting. But on a cash flow statement, it belongs in the liability column. It does not produce income. It consumes income. The mortgage is listed separately as a liability, but so is the ongoing expense of ownership that never appears on the balance sheet: the taxes paid, the repairs made, the utilities consumed, the insurance premiums written.

When someone understands this — truly understands it — their entire approach to financial planning shifts. Rather than pouring excess income into paying down a mortgage faster (building equity in a liability), they redirect income toward acquiring cash-flowing assets: rental properties, businesses, dividend-producing stocks and options strategies, or commodities. Those assets generate income. That income can then fund lifestyle expenses — including the home.

That is the Rich Dad model. Let assets pay for liabilities. Do not confuse the two.Cash flow vs. appreciation: Choosing the right strategy

The five asset classes that actually build wealth

If the primary residence is a liability, where should wealth-building attention go? Rich Dad points to four primary asset classes, each of which can generate cash flow when properly invested in:

- Real estate (investment properties)

Rental properties where tenant income covers all expenses and generates positive monthly cash flow. This is the asset class Robert Kiyosaki built his foundational wealth in, and it remains the starting point for most Rich Dad investors. Learn more on the Real Estate investing page. - Business

A system or enterprise that generates income independently of the owner’s active labor. The B-quadrant business — one that operates without requiring the owner’s daily presence — is a cash-flowing asset. Entrepreneurship education is a core focus of the Rich Dad curriculum. - Paper assets

Stocks, bonds, options, and other securities. When used for cash flow — through dividend strategies, covered calls, and other techniques — paper assets can generate consistent monthly income. Rich Dad’s stocks and paper assets education covers these strategies in depth. - Commodities

Gold, silver, oil, gas, and other physical resources. Robert Kiyosaki is a longtime advocate for precious metals — particularly physical gold and silver — as stores of value and protection against currency debasement. Rich Dad strongly favors ownership of physical metals over paper proxies such as ETFs. - Cryptocurrency

A decentralized digital currency that you can buy, sell or exchange directly — and it’s not backed by the government or any issuing institution. It seems everyone is talking about digital currencies like Bitcoin, Ethereum, Tron, and Litecoin (there are more than 5,000 cryptocurrencies in existence today) these days. And why not? With massive fluctuations in value and short-term gains in the 1000% range, it’s very exciting and enticing stuff.

Each of these asset classes is something worth investing in. A primary home is not on this list — not because homeownership is wrong, but because a home is not an investment vehicle in the way these assets are.

Should you still buy a home?

None of this means homeownership is a bad decision. It means homeownership should be understood clearly — as a lifestyle choice and a place to live, not as a financial strategy.

There are real benefits to owning a home. Stability. Control over a living space. The option to sell at some point in the future. Emotional satisfaction. These are legitimate reasons to own rather than rent. Rich Dad does not argue against them. What Rich Dad argues against is the financial illusion: the idea that the mortgage payment is building wealth in the way that acquiring a cash-flowing asset builds wealth.

According to iPropertyManagement research, the average homeowner’s net worth is substantially higher than the average renter’s — but much of that difference is home equity, which is illiquid and requires selling the home to access. The median renter’s net worth is dramatically lower not because renting builds less wealth, but because most renters are not aggressively deploying the capital they are not tying up in home equity into income-producing assets. The Rich Dad approach would have those renters — or homeowners — investing in assets that generate monthly cash flow, using that cash flow to fund lifestyle and using remaining income to acquire more assets.

The goal is financial freedom: the point at which passive income from assets permanently covers monthly living expenses. A primary residence cannot get anyone to that point. Investment real estate, businesses, and cash-flowing paper assets can. Understanding the difference between the two is the first step.The five asset classes that actually build wealth

The truth sets you free

The financial advice most people receive — from well-meaning parents, optimistic real estate agents, and credentialed financial planners — includes the idea that buying a home is the cornerstone of financial security. Rich Dad does not dispute that a home can provide security, comfort, and stability. What Rich Dad disputes is the label: calling that home an asset when the cash flow test shows it is a liability is not a semantic difference. It is the difference between a financial strategy that works and one that keeps people on a treadmill their entire working lives.

Robert Kiyosaki’s rich dad — the man who built real wealth through financial education — drew a clear line. Assets put money in your pocket. Liabilities take money out. Your house, as long as you are living in it and paying for it, takes money out. That is the truth. And as Rich Dad has always taught, the truth sets people free.

The next step is not to sell the house. It is to start acquiring assets — real estate that tenants pay for, businesses that run without the owner, investments that produce monthly income — until those assets generate enough cash flow to cover all expenses, including the home. That is the path to financial freedom. And it begins with seeing the financial world as it actually is.

FAQs

Under standard accounting definitions, a house is listed as an asset because it has value. But Rich Dad uses a cash flow definition: an asset puts money in your pocket, and a liability takes money out. Under that definition, a primary residence — which costs money every month in mortgage payments, taxes, insurance, maintenance, and utilities — is a liability. It only becomes an asset if it generates income that exceeds all expenses, which happens with investment property, not a personal home.

Robert Kiyosaki defines assets by cash flow, not accounting convention. A primary home generates no monthly income. Every month, it removes money from the owner’s pocket through housing costs. It cannot put money in the owner’s pocket unless it is sold (realizing appreciation, which is not guaranteed) or rented out (generating passive income). Rich Dad’s position is that calling a home an asset creates a false sense of financial security and diverts attention from the true wealth-building vehicles: income-producing investments.

Yes — under specific conditions. An investment property that generates positive cash flow after all expenses (mortgage, taxes, insurance, and maintenance) qualifies as an asset because it puts money in the owner’s pocket each month. House hacking — renting out rooms or units within a personal residence — can also partially convert a liability into an asset to the degree that rental income offsets ownership costs. But a home that is fully occupied by the owner and produces no income remains a liability by the Rich Dad definition regardless of its market value.

Rich Dad identifies four primary asset classes: real estate (investment properties generating cash flow), business (systems that produce income independent of the owner’s labor), paper assets (stocks, bonds, options, and other securities used for income generation), and commodities (gold, silver, oil, gas, and other physical resources). Each of these can be structured to produce monthly income. A primary residence produces none. Learn more about investing across these asset classes at Rich Dad’s investing education hub.

Home equity represents the difference between what a property is worth and what is owed on it. While equity does grow over time (as the mortgage is paid down and if the market appreciates), equity is illiquid — it cannot be spent or invested without selling the home or borrowing against it. It does not generate monthly income. Rich Dad distinguishes between paper wealth (equity on a balance sheet) and real wealth (cash flow that funds daily life). Building equity in a liability is not the same as building cash-flowing assets.

Not necessarily. Rich Dad’s message is not to abandon homeownership — it is to understand homeownership clearly. A home provides genuine benefits: stability, security, community, and the satisfaction of ownership. The Rich Dad recommendation is to acquire income-producing assets alongside the home, so that those assets generate enough cash flow to cover all living expenses including housing costs. The goal is financial freedom, not rental arbitrage. Own a home if it serves your life — just do not confuse it with the investments that will actually set you free.

Rich Dad teaches that real estate investing — specifically income-generating rental property — is one of the most powerful wealth-building vehicles available. The key principle is investing for cash flow first: selecting properties where rental income exceeds all expenses, including mortgage, taxes, insurance, and maintenance. Appreciation is treated as a secondary benefit, not the primary strategy. Advanced techniques like the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat) allow investors to recycle capital across multiple properties while building a portfolio of cash-flowing assets. Explore the full approach at Rich Dad’s real estate investing guide.