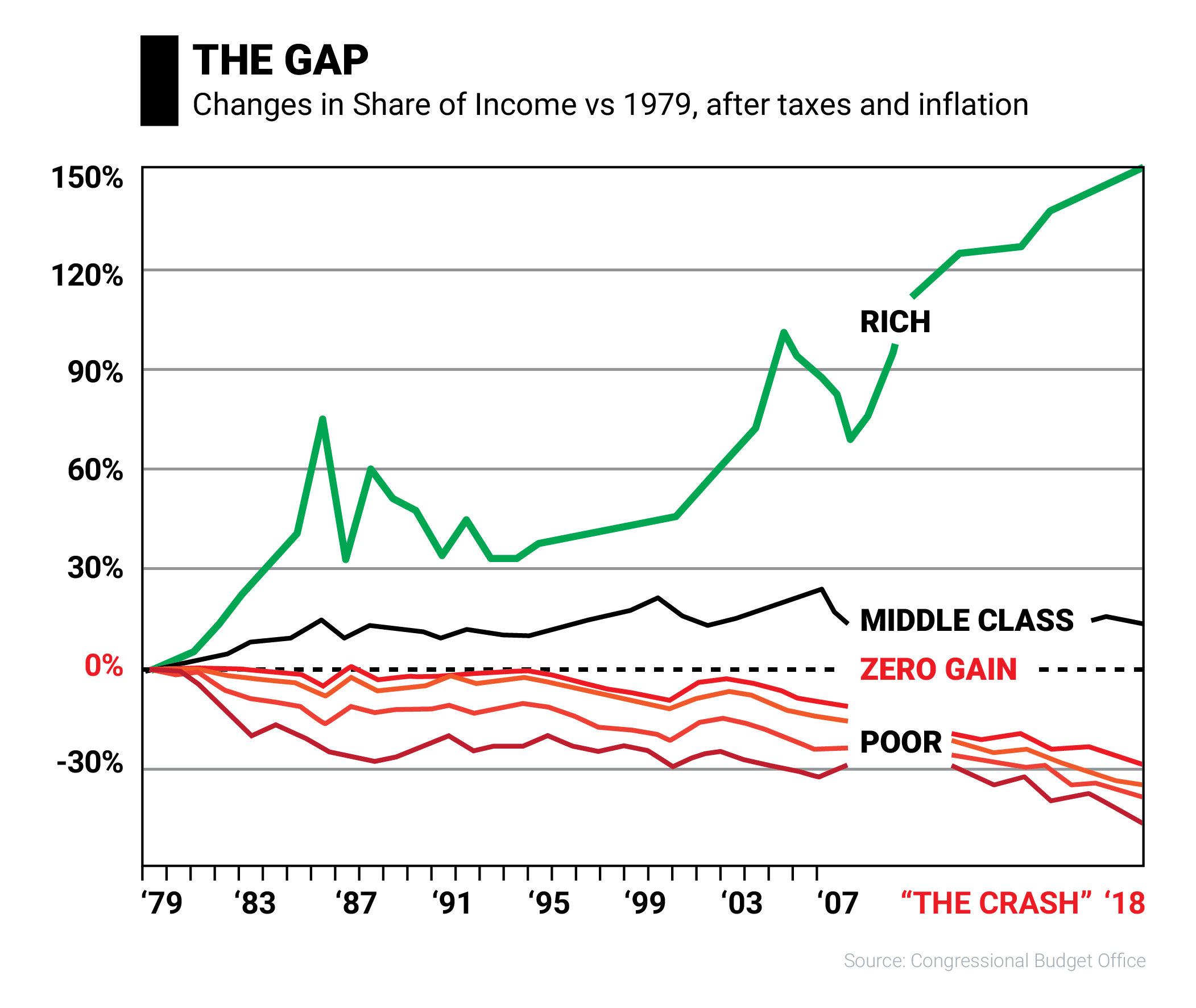

This chart shows that over the last nearly four decades, the rich have gotten massively richer while the poor and the middle class have gotten much poorer.

How could this happen?

The answer lies in fake assets.

What are fake assets?

Historically, the conventional financial advice given by people was, “Go to a good school, get a good job, save money, buy a house, and invest in a balanced portfolio of stocks, bonds, and mutual funds.” That was the advice Robert Kiyosaki’s poor dad, his natural father, gave him. It’s likely you were given this advice as well.

Robert’s rich dad, his best friend’s father, however, didn’t buy into this advice because he knew something had changed.

It began when Nixon took the dollar off the gold standard in 1971. After that, our money was toxic. It became debt.

After realizing what the government was up to, rich dad came up with his #1 lesson, which is: “The rich do not work for money.” Rich dad realized money was toxic, designed to steal the wealth of anyone who worked for money, saved money, or invested money in government sponsored investments such as 401(k)s, IRAs, stocks, mutual funds, and ETFs.

In 1997, Robert shared his rich dad’s advice with the world by publishing his book, Rich Dad Poor Dad. In that book he wrote the following truths:

“Your house is not an asset.”

“Savers are losers.”

“The rich do not work for money.”

The so-called financial experts howled. To them, this was heresy. “You don’t know what you’re talking about,” they said. Unfortunately, Robert did. And many recessions that have wiped out the wealth of millions proves so. Also unfortunate, is that even though “Rich Dad Poor Dad” is the best-selling personal finance book of all time with over 32 million copies sold, millions upon millions more have never read the book and are suffering financially today.

In that book, Robert shared rich dad’s simple formula for assets versus liabilities.

“An asset puts money in your pocket,” said rich dad. “A liability takes money out of your pocket.”

The simple definition of a fake asset is one that promises to make you richer but in actuality robs you blind.

Types of fake assets

A 401(k) is a fake asset because cash keeps flowing out of your pocket… for years. An Individual Retirement Account, or IRA, is a fake asset because it takes money out of your pocket… for years.

A government pension is a fake asset because it is taking money out of your pocket… also for years.

A house that is a primary residence is a fake asset because it is taking money out of your pocket in the form of a mortgage for 30 or more years. You also have to pay for all the repairs and taxes, out of pocket.

A mutual fund is a fake asset. So are stocks, bonds, ETFs, and savings. They are all derivatives. Mutual funds are loaded with fees – fees that make the rich richer, and you poorer. Insiders know, mutual fund investors put up 100 percent of the money, take 100 percent of the risk, yet gain less than 20 percent of the profits.

Remember: Assets put money in your pocket. Liabilities take money from your pocket. By following this simple formula, you can always tell the difference between a fake and a real asset.

What’s the problem with fake assets?

As mentioned at the beginning of this post, the rich have gotten massively richer while the poor and the middle class have suffered over the last nearly four decades.

The way in which the rich are getting so incredibly rich is by using fake assets to steal the wealth of the poor and the middle class.

That is the problem with fake assets. And it’s a growing one. But first, a quick history lesson.

In 1974, the Employee Retirement Income Security Act, which protected employees’ company pensions, went into effect. Four years later, 401(k), another financially engineered retirement program, got its beginnings.

There was a problem with this. Suddenly non-investors, men and women without any financial education, were expected to become investors. That was the start of a massive financial rip-off by “too big to fail” banks, the U.S. government, and Wall Street.

The institution of the 401K gave birth to an entire industry of so-called financial planners who are really professional salespeople trained to sell paper assets like stocks, bonds, and mutual funds for commission. To be clear, these are not investments. They are products that banks, the U.S. government, and Wall Street want to sell to become rich. They do so through fees, and they prop up growth by selling more products. If that sounds like a Ponzi scheme to you, you’re on to something.

Yet, despite a massive industry of financial planners, rising stock markets, and millions of people investing in instruments like 401K’s and IRA’s, as we see, the rich are getting richer and the poor and the middle class are getting poorer.

That is the problem with fake assets.

The coming collapse of the US dollar

If you’ve read Robert’s other book, Conspiracy of the Rich: The 8 New Rules of Money, you know that many people think of the dollar as money, but since Nixon moved the dollar from the gold standard, the dollar is no longer money – it’s a currency. This is the reason we’ve had so many wild economic swings in the last four decades.

The dollar is no longer an asset that can be considered a safe-haven for investors in times of uncertainty. Because it’s a currency, it’s affected by the wild swings of the market just like any other asset class. In 2022 alone, the dollar has swung from $1.51 versus the Euro to its recent low against the Euro of $1.23. Because the dollar is a tradable currency, it’s subject to huge gains—and drops—in value based on market whims. As such, it gains and loses value all the time.

US deficit spending

In 2022, the government spent $1.38 trillion more than it collected.

To the average person, this is insane. Everyone knows what happens when you spend more than you earn for years, your creditors come knocking on your door and people refuse to believe you when you say you’ll pay them back.

Today, investors are saying they don’t believe that the US can pay back their creditors. That is why they’re ditching the dollar.

US foreign debt

As of 2025, The United States owes China approximately $749 billion, while Japan has the top spot among foreign creditors at $1.1 trillion. These numbers indicate that we’re much more indebted to the rising global economic power of China that the layman may have previously thought. The US is the biggest debtor nation in the world, and we’re indebted most to a country that has expressed continued and stronger criticism of the dollar. If China decides to collect on its debt, the dollar would completely collapse.

This is another reason why investors are ditching the dollar.

Living on borrowed time

History, as always, is destined to repeat itself unless patterns change. Many financial experts believe our country is in for another major US-style deflation and German-style hyperinflation. Meaning, if things continue as they are, we’re in for both types of depressions. Ultimately, the dollar may gain strength for a little while, but will eventually become toast.

As the old saying goes, all currencies eventually go to zero.

There is no currency in the history of the world that hasn’t eventually crashed under the burdens of debt that its government heaped upon it. The dollar will be no exception. It’s just a matter of time—and it’s possible that time will be sooner rather than later. Those who are betting on the dollar are living on borrowed time.

The dollar is not a safe asset. Eventually, once the crisis has seemingly subsided, all those dollars that have been pumped into the economy by the Fed will flood into the market and cause severe inflation. The middle-class will likely be devastated as years and years worth of savings lose value. When that happens, the last thing you want to be holding is dollars.

So, what is safe?

All of this begs the question, if the dollar isn’t safe, what is?

The short answer is cash flowing assets.

The investment philosophy of the rich – like Robert Kiyosaki – is simple. They invest in assets that have cash flow and hedge against inflation, things like businesses, real estate, oil wells, and more.

Additionally, they keep their liquid investments in gold and silver instead of dollars. This is because gold and silver rise when the dollar falls.

For those who aren’t financially educated, this may not be safe. This kind of investing takes a high level of financial education. You have to decide for yourself where your safe harbor is.

What you can do

The rich do not invest in fake assets and they do not work for money. Rather they know the rules of the game now that money is debt. Their financial knowledge and intelligence allow them to invest in real assets that put money in their pockets each month and make them richer.

If you want to get off the hamster wheel of giving your money away to the rich through fake assets, you must first start with financial education. You must increase your financial intelligence to invest in real assets that provide cash flow and understand the following:

- How to use taxes to acquire assets.

- How to use debt to acquire assets.

- How to reinvest gains without paying taxes.

- Why it makes sense to save gold and silver, not fake money.

By increasing your financial education and knowledge, you too will be able to invest like the rich and easily spot fake assets when you see them…and invest in real assets like a pro.